ACCT 2301 Chapter Notes -Indirect Costs, Continual Improvement Process, Financial Statement

4 Feb 2014

School

Department

Course

Professor

Document Summary

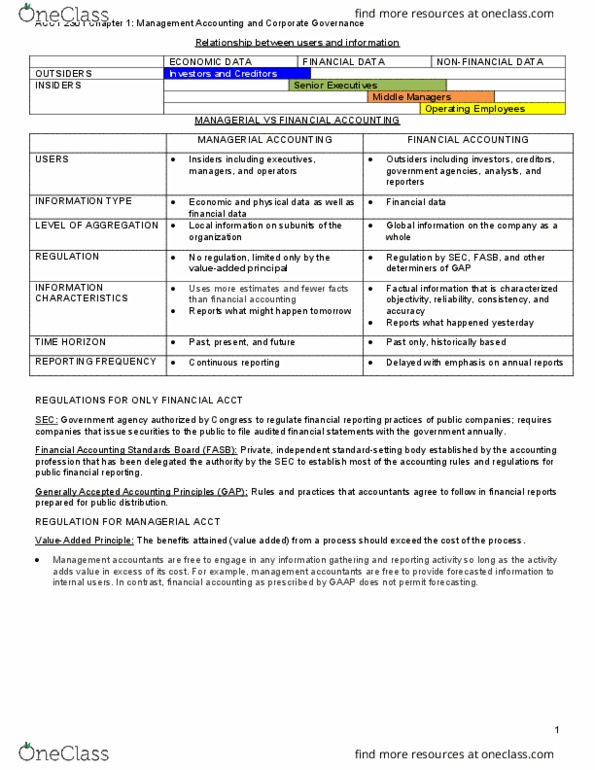

Info to plan, direct, and control busn operation. Info is related to employees" job level. Lower level nonfinancial info such as work schedules, store hours, customer service policies, etc. Midlevel managers get a mix of nonfinancial and financial info. Managerial detailed info on specific subunits of a company. Financial global info that reflects performance of a company as a whole. Sec delegates authority to fasb, which creates gaap. No need to protect public interest (except for financial data, info generated by manag acct is not available to public), therefore less regulation. Only restricted by the value-added principle gather and report info if value added is greater than the cost. Financial objectivity, reliability, consistency, and historic in nature. Managerial relevance, timeliness; more estimates, fewer facts. Managerial can"t wait until end of year to discover problems; continuous basis. Overhead (utilities, rent on manufacturing facilities, supervisors, depreciation, etc) * if products are stored, these costs are part of inventory until sold.