FINA 2201 Chapter Notes - Chapter 2: Economic Equilibrium, Financial Industry Regulatory Authority, Bid Price

16 Dec 2016

School

Department

Course

Professor

Document Summary

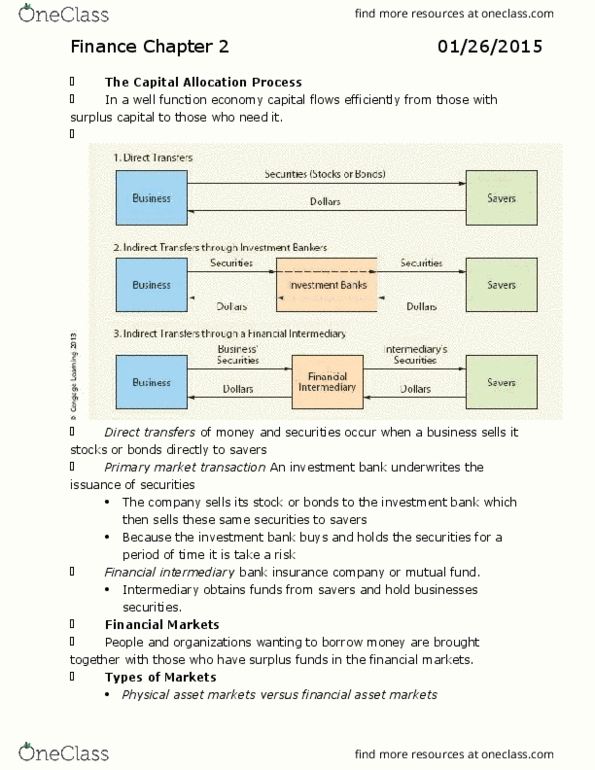

Physical/tangible/real asset markets: are for products such as wheat, autos, real estate, computers, and machinery. Financial asset markets: deal with stocks, bonds, notes, and mortgages and derivative securities whose values are derived from changes in the prices of other assets. Spot markets: the markets in which assets are bought or sold for on-the-spot delivery. Futures markets: the markets in which participants agree today to buy or sell an asset at some future date. Such a transaction can reduce, or hedge, the risks faced by both the farmer and the food processor. Money markets: the financial markets in which funds are borrowed or loaned for short periods (less than one year). Capital markets: the financial markets for stocks and for intermediate (1-10 years) or long-term debt (10+ years) Primary markets: markets in which corporations raise capital by issuing new securities. Secondary markets: markets in which securities and other financial assets are traded among investors after they have been issued by corporations.