ECON 2001.02 Chapter Notes - Chapter 9: Economic Equilibrium, Perfect Competition, Marginal Revenue

5 Oct 2018

School

Department

Course

Professor

Document Summary

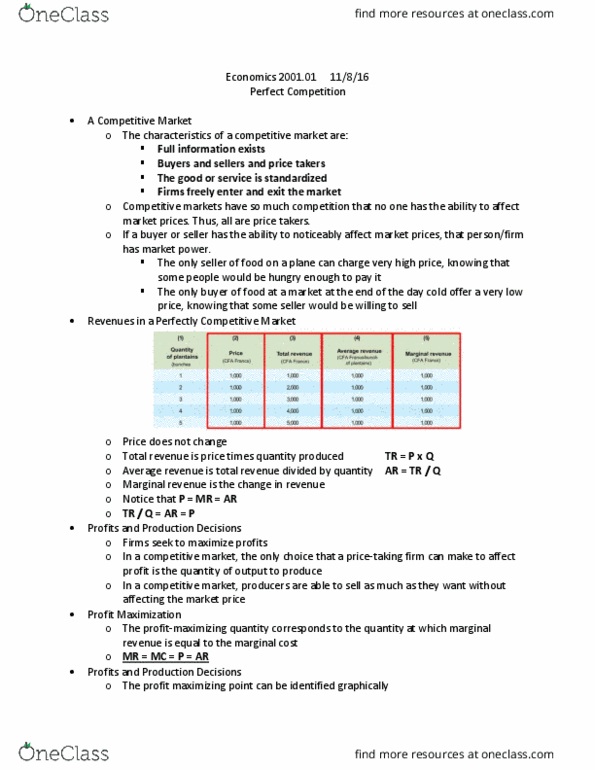

It is impossible for any single buyer or seller to unilaterally change the price of any product. Prices are determined by the overall interaction of supply and demand in a market. A market clearing price is the same as equilibrium price, such that they are both defined as the price where qs = qd. An individual firm"s demand curve is flat at the equilibrium price. Competitive firms must make the following decisions: whether to enter, stay, or leave the industry, whether to produce or temporarily shut down, how much to produce. Total revenue = price quantity ; average revenue = total revenue quantity. Ar = (tr q) = {(p q) q} = p. Marginal revenue = change in total revenue change in quantity. The slope of the total revenue graph is equilibrium price. If a firm"s p > atc, the firm is making + . If a firm"s p = atc, the firm is making 0 .