FIN 360 Chapter Notes - Chapter 2: Accounts Payable, Current Liability, Accrued Interest

18 Oct 2016

School

Department

Course

Professor

Document Summary

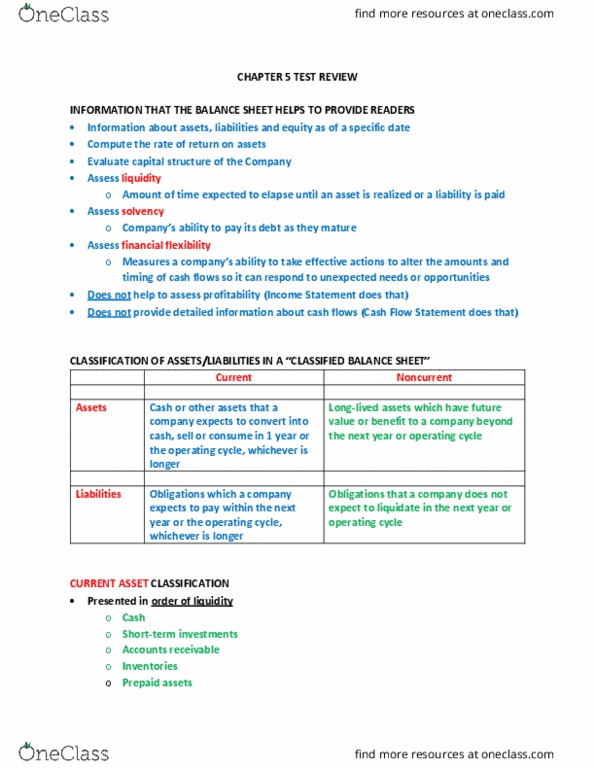

Assets must possess two characteristics to be report on balance sheet: it must be owned (or controlled0 by the company, it must confer expected future economic benefit that result from a past transaction or event. Lists assets in the order of decreasing liquidity. Liquidity refers to the ease of converting noncash assets into cash. Historical cost assets that are reported at their original acquisition costs and not the market value. Only report intangible assets on the balance sheet when the assets are purchased. Represents the sources of capital the company uses to finance the acquisition of assets. Equity represents capital that has been invested by stockholders directly purchase of stock or a form of retained earnings that is reinvested in the business and not paid out as dividends. Net working capital reflects the difference between current assets and current liabilities and is defined as follows: Net working capital = current assets current liabilities.