ACTG 2300 Chapter Notes - Chapter 5: Operating Leverage, Earnings Before Interest And Taxes, Contribution Margin

7 Nov 2017

School

Department

Course

Professor

Document Summary

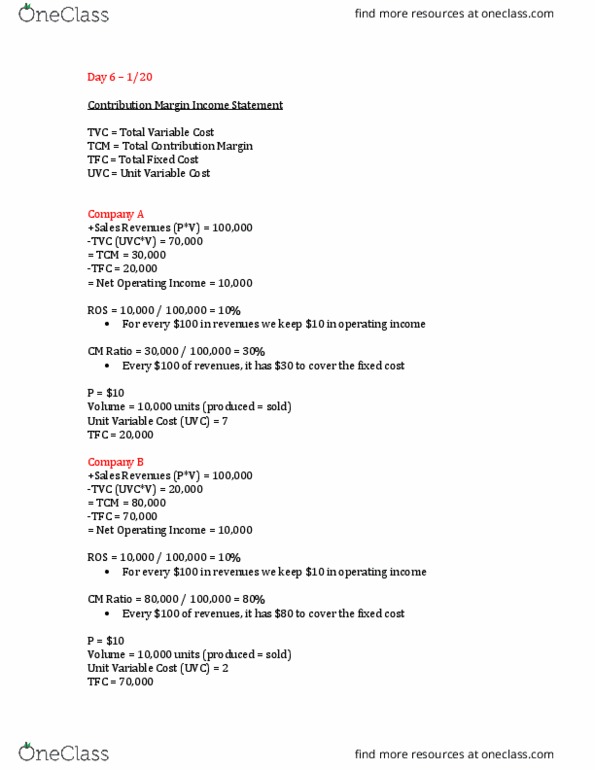

Contribution margin the amount remaining from sales revenue after variable expenses have been deducted: the amount available (first) to cover fixed expenses and then (second) to provide profits for the period. Break-even point the level of sales at which profit is zero: once the break-even point has been reached, net operating income will increase by the amount of the unit contribution margin for each additional unit sold. Profit = (sales variable expenses) fixed expenses. Sales = (selling price per unit) x (quantity sold) Variable expenses = (variable expenses per unit) x (quantity sold) Profit = (p x q v x q) fixed expenses. Contribution margin ration a percentage of sales. Cm ratio = contribution margin / sales: shows how the contribution margin will be affected by a change in total sales, example cm ratio = 40%. Application for each dollar increase in sales, total contribution margin will increase by 40 cents.