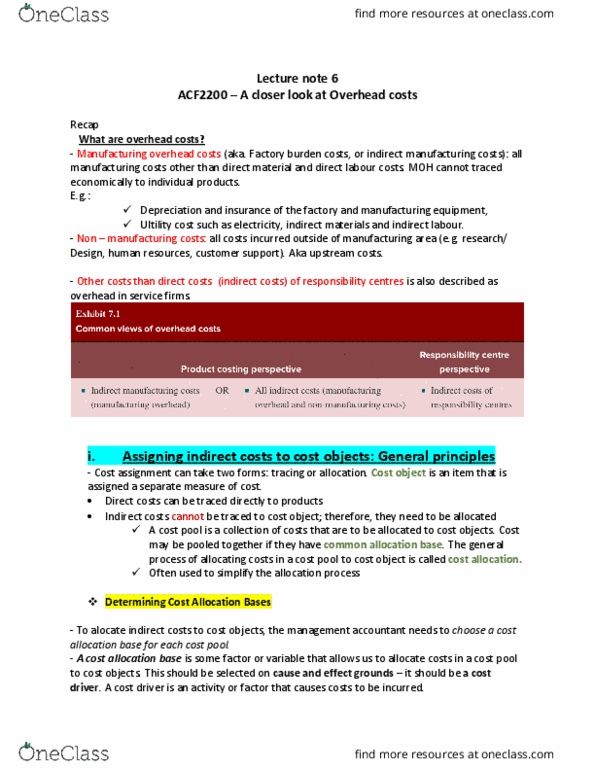

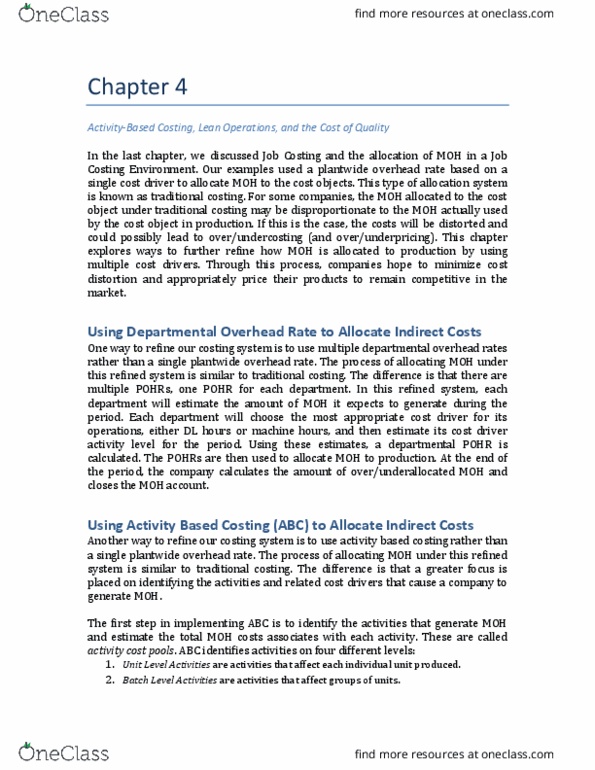

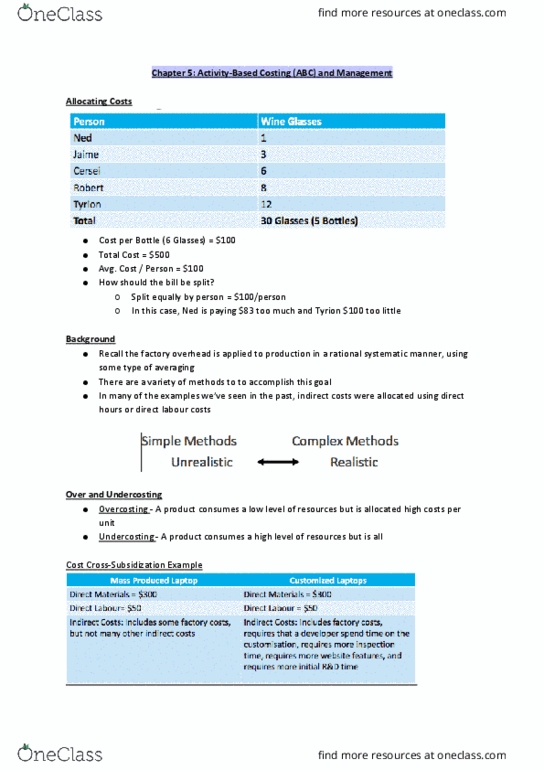

ACG 2071 Chapter Notes - Chapter 4: Cost Driver, Lean Manufacturing, American Express

Get access

Related Documents

Related Questions

AirComp Corporation produces component parts for the aircraftindustry. In prior years, they maintained a job-costing systemconsisting of direct materials and direct labor cost andmanufacturing overhead. Manufacturing overhead was allocated toproduction jobs using a single-indirect cost allocation rate, whichwas $115 per direct labor hour.

For 20x1, the Company decided to change the method of allocatingmanufacturing overhead to production jobs from the single-indirectcost allocation approach to the activity-based costing (âABCâ)indirect cost allocation approach. For purposes of developing theABC allocation rates, AirCompâs cost accounting team prepared thefollowing analysis:

Activity | Cost Driver | Allocation Rate |

Material handling | Parts handled | $0.40 |

Lathe work | No. of lathe turns | $0.20 |

Milling | Machine hours | $20.00 |

Grinding | No. of parts ground | $0.80 |

Testing | No. of units tested | $15.00 |

For 20x1, AirCompâs cost accountant team prepared the followinganalysis of the direct costs and indirect cost activities for Job100 and Job 200, the only production jobs in process for theperiod:

Job 100 | Job 200 | |

Direct materials cost | $9,700 | $59,900 |

Direct labor cost | $750 | $11,250 |

No. of direct manufacturing labor hours | 25 | 375 |

No. of parts ground | 500 | 2,000 |

No. of lathe turns | 20,000 | 60,000 |

Machine hours | 150 | 1,050 |

No. of units produced during period (all are tested) | 10 | 200 |

Required

1.For each job, determine total per unit cost using direct laborhours to allocate manufacturing overhead to each job.

2.For each job, determine total per unit cost using anactivity-based costing approach to allocate manufacturing overheadcost to job.

3.Compare the per unit cost figures for each job computed instep a. and step b., above. Why do the new ABC approach differ fromthe single-indirect cost allocation systems differ in the amount ofthe per unit indirect cost allocated to each job (i.e. what was theimplications of the cost allocation method change on the amount ofper unit cost allocated to each job and what factors caused theobserved changes).

4.How might AirComp Corporation use the information from ABCallocation approach to better manage its business, i.e. what arethe advantages of using an activity-based costing approach?

Ramsey Company produces speakers (Model A and Model B).Ramseyâs controller, Mr. Jacks, is evaluating the different methodsof allocating manufacturing overhead to the products. Both productspass through two producing departments. Model Aâs production ismuch more labor-intensive than that of Model B. Model B is alsomore popular of the two speakers. The following data have beengathered for the two products.

Product Data | ||||

Model A | Model B | |||

Units produced & sold per year | 20,000 | 200,000 | ||

Sales Revenue | $600,000.00 | $6,000,000.00 | ||

Prime cost | $100,000.00 | $1,000,000.00 | ||

Direct Labor Hours | 140,000 | 300,000 | ||

Machine hours | 20,000 | 180,000 | ||

Set Ups | 40 | 160 | ||

Inspection runs | 600 | 1,400 | ||

Packing Orders | 9,000 | 81,000 | ||

Estimated Manufacturing Overhead: | ||||

Machining costs | $160,000.00 | |||

Setup costs | $180,000.00 | |||

Inspection costs | $140,000.00 | |||

Packing costs | $180,000.00 | |||

Total Manufacturing Overhead | $660,000.00 | |||

Suppose that Ramsey decides to use departmental overhead rates.There are two departments: Department 1 (machine intensive) with anMOH rate of $2.75 per machine hour and Department 2 (laborintensive) with an MOH rate of $1.25 per direct labor hour. Theactual consumption of these two drivers is as follows:

Department 1 | Department 2 | |

Machine Hours | Direct Labor Hours | |

Model A | 55,000 | 110,000 |

Model B | 145,000 | 330,000 |

Compare the results for the simple cost allocation system(plant-wide), departmental cost allocation and the ABC costallocation systems. Which do you think is more accurate and why? What circumstances would favor Ramseyadopting ABC as their allocation method (provide at least threereasons)?