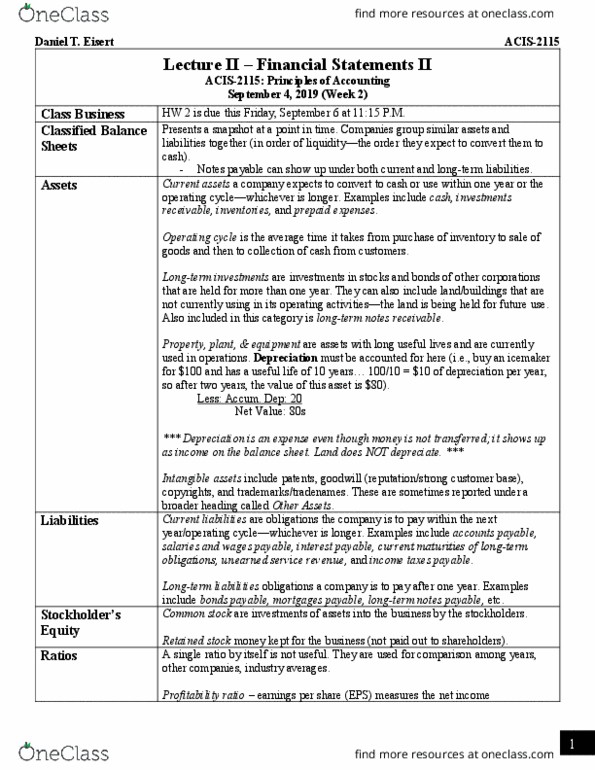

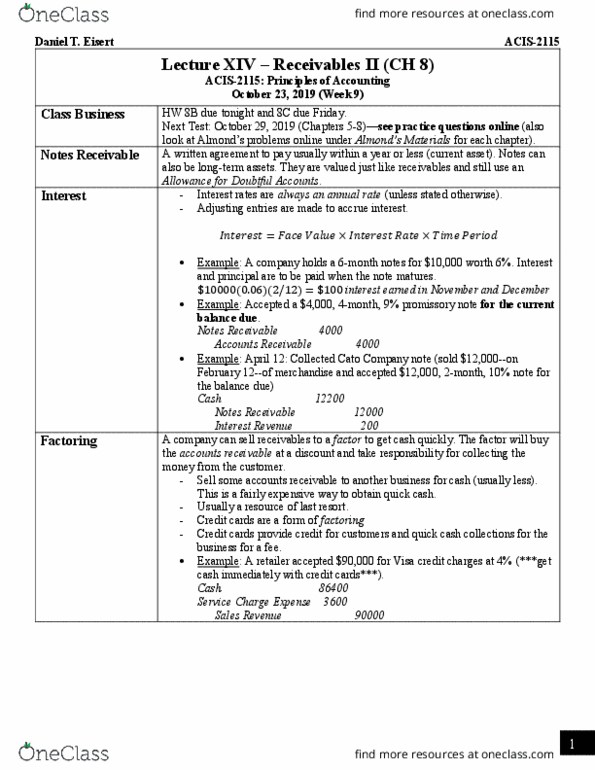

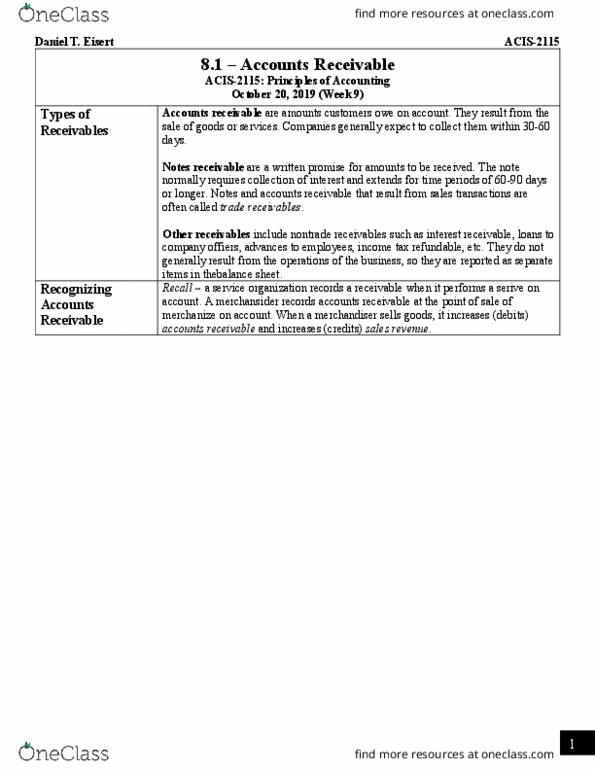

ACIS 2115 Chapter Notes - Chapter 8.3: Accounts Receivable

Get access

Related Documents

Related Questions

Select the term that best fits each of the following definitions and descriptions.

| a. | Notes receivable |

| b. | Nontrade receivables |

| c. | Net realizable value |

| d. | Direct write-off method |

| e. | Interest-bearing note |

| f. | Maturity date |

| g. | Promissory note |

| h. | Factoring receivables |

| i. | Trade discount |

| j. | Present value |

| k. | Allowance method |

| l. | Sales discount |

| m. | Negotiable note |

| n. | Non-interest-bearing note |

| o. | Assignment of receivables |

| p. | Valuation date |

____ 21. Receivables that are evidenced by a formal written promise to pay a certain sum of money at a specified date.

____ 22. The date the principal amount of a note is due to be paid.

____ 23. The sum of future receipts or payments discounted to the present date at an appropriate rate of interest.

____ 24. A method of recognizing the estimated losses from uncollectible accounts as expenses during the period in which the sales occur.

____ 25. A note that is legally transferable by endorsement and delivery.

____ 26. Any receivable arising from transactions that are not directly associated with the normal operating activities of a business.

____ 27. A note written in the form where the face amount includes the interest charges.

____ 28. The borrowing of money with receivables pledged as security on the loan.

____ 29. A note written in the form where the maker promises to pay the face amount plus interest at a specified rate.

____ 30. An unconditional written promise to pay a certain sum of money at a specified time.

Flush Mate Co. wholesales bathroom fixtures. During the current fiscal year, Flush Mate Co. received the following notes:

| Date | Face Amount | Interest Rate | Term | |

|---|---|---|---|---|

| 1. | Mar. 6 | $84,500 | 6% | 45 days |

| 2. | Apr. 23 | 21,700 | 9% | 60 days |

| 3. | July 20 | 43,900 | 5% | 120 days |

| 4. | Sept. 6 | 51,500 | 6% | 90 days |

| 5. | Nov. 29 | 30,600 | 5% | 60 days |

| 6. | Dec. 30 | 71,300 | 6% | 30 days |

| Required: | |

| 1. | Determine for each note (a) the due date and (b) the amount of interest due at maturity, identifying each note by number. Assume a 360-day year when calculating interest.(Note: Round each interest computation to the whole dollar.) |

| 2. | Journalize the entry to record the dishonor A note receivable is dishonored when the maker of the note fails to pay the note on the due date. of Note (3) on its due date. Refer to the Chart of Accounts for exact wording of account titles. Assume a 360-day year when calculating interest. Round your answer to the nearest whole dollar. |

| 3. | Journalize the adjusting entry to record the accrued interest on Notes (5) and (6) on December 31. Refer to the Chart of Accounts for exact wording of account titles. Assume a 360-day year when calculating interest. Round your answer to the nearest whole dollar. |

| 4. | Journalize the entries to record the receipt of the amounts due on Notes (5) and (6) in January. Refer to the Chart of Accounts for exact wording of account titles. Assume a 360-day year when calculating interest. Round your answer to the nearest whole dollar. |

2

X

Chart of Accounts

| CHART OF ACCOUNTS | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Flush Mate Co. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| General Ledger | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

none

X

Starting Question

Shaded cells have feedback.

1. Determine for each note (a) the due date and (b) the amount of interest due at maturity, identifying each note by number. Assume a 360-day year when calculating interest. (Note: Round each interest computation to the whole dollar.)

| Note | Due Date | Interest Due at Maturity |

|---|---|---|

| 1. | selector 1Apr. 20 June 22 Apr. 21 Apr. 20 June 9 Apr. 30 | |

| 2. | selector 2June 22 July 22 June 23 June 22 July 25 June 30 | |

| 3. | selector 3Nov. 17 Dec. 5 Nov. 20 July 1 Nov. 17 July 31 | |

| 4. | selector 4Dec. 5 Dec. 4 Dec. 5 Oct. 31 Dec. 6 Dec. 1 | |

| 5. | selector 5Jan. 28 Sep. 29 Jan. 29 Jan. 28 Nov. 28 Nov. 17 | |

| 6. | selector 6Jan. 29 Nov. 28 Jan. 30 Jan. 29 Nov. 17 Jan. 28 |

Points:

12 / 12

Feedback

Check My Work

Count the number of days in each month until the total number of days is reached for the term of the note and this will be the due date. Interest is not charged on the first day of the note.

Explanation

none

X

Journal

Shaded cells have feedback.

2. Journalize the entry to record the dishonor

A note receivable is dishonored when the maker of the note fails to pay the note on the due date.

of Note (3) on its due date. Refer to the Chart of Accounts for exact wording of account titles. Assume a 360-day year when calculating interest. Round your answer to the nearest whole dollar.How does grading work?

The grader is designed to give you the best score possible, even when you skip lines or enter them out of order. It does this by taking every line you have entered and comparing it to every line in the answer. When it finds the line that gives you the best score, it considers that a match.

PAGE 1

JOURNAL

ACCOUNTING EQUATION

Score: 37/37

| DATE | DESCRIPTION | POST. REF. | DEBIT | CREDIT | ASSETS | LIABILITIES | EQUITY | |

|---|---|---|---|---|---|---|---|---|

| 1 | â | â | â | â | ||||

| 2 | â | â | â | |||||

| 3 | â | â | â |

Solution

| DATE | DESCRIPTION | POST. REF. | DEBIT | CREDIT | ASSETS | LIABILITIES | EQUITY | |

|---|---|---|---|---|---|---|---|---|

| 1 | ||||||||

| 2 | ||||||||

| 3 |

Points:

7 / 7

3. Journalize the adjusting entry to record the accrued interest on Notes (5) and (6) on December 31. Refer to the Chart of Accounts for exact wording of account titles. Assume a 360-day year when calculating interest. Round your answer to the nearest whole dollar.

How does grading work?

The grader is designed to give you the best score possible, even when you skip lines or enter them out of order. It does this by taking every line you have entered and comparing it to every line in the answer. When it finds the line that gives you the best score, it considers that a match.

PAGE 1

JOURNAL

ACCOUNTING EQUATION

Score: 21/25

| DATE | DESCRIPTION | POST. REF. | DEBIT | CREDIT | ASSETS | LIABILITIES | EQUITY | |

|---|---|---|---|---|---|---|---|---|

| 1 | â | â | â | |||||

| 2 | â | â |

Solution

| DATE | DESCRIPTION | POST. REF. | DEBIT | CREDIT | ASSETS | LIABILITIES | EQUITY | |

|---|---|---|---|---|---|---|---|---|

| 1 | ||||||||

| 2 |

Points:

4.2 / 5

4. Journalize the entries to record the receipt of the amounts due on Notes (5) and (6) in January. Refer to the Chart of Accounts for exact wording of account titles. Assume a 360-day year when calculating interest. Round your answer to the nearest whole dollar.

All transactions on this page must be entered (except for post ref(s)) before you will receive Check My Work feedback.

PAGE 1

JOURNAL

ACCOUNTING EQUATION

Score: 2/99

| DATE | DESCRIPTION | POST. REF. | DEBIT | CREDIT | ASSETS | LIABILITIES | EQUITY | |

|---|---|---|---|---|---|---|---|---|

| 1 | ||||||||

| 2 | ||||||||

| 3 | ||||||||

| 4 | ||||||||

| 5 | ||||||||

| 6 | ||||||||

| 7 | ||||||||

| 8 |

Solution

| DATE | DESCRIPTION | POST. REF. | DEBIT | CREDIT | ASSETS | LIABILITIES | EQUITY | |

|---|---|---|---|---|---|---|---|---|

| 1 | ||||||||

| 2 | ||||||||

| 3 | ||||||||

| 4 | ||||||||

| 5 | ||||||||

| 6 | ||||||||

| 7 | ||||||||

| 8 |

Points:

0.36 / 18

Feedback

Check My Work

2.

Typically, the maker of a dishonored note fails to pay the note on the due date. A company that holds a dishonored note transfers the face amount of the note plus any interest due back to an accounts receivable account. Interest revenue is not dependent on receiving the interest at this point.

3.

(Note 5) Calculate the number of days of interest that accrues between November 29 and December 31. Remember interest is not charged on the first day of the note. Use this to calculate:

(a) Interest rate x face amount = annual interest.

(b) Annual interest x (number of days to end of year ÷ 360 days) = interest on note to the end of the year

Two accounts related to interest are used for the transaction.

(Note 6) Calculate the number of days of interest that accrues between December 30 and December 31. Remember interest is not charged on the first day of the note. Use this to calculate:

(a) Interest rate x face amount = annual interest.

(b) Annual interest x (number of days to end of year ÷ 360 days) = interest on note to the end of the year

Two accounts related to interest are used for the transaction.

4.

Cash received will include the maturity value of the note.

Explanation

1

Ã

Need help with part 3 and 4 please.