ACCG100 Lecture Notes - Lecture 6: General Ledger, Retained Earnings, Sole Proprietorship

15 Aug 2018

School

Department

Course

Professor

Document Summary

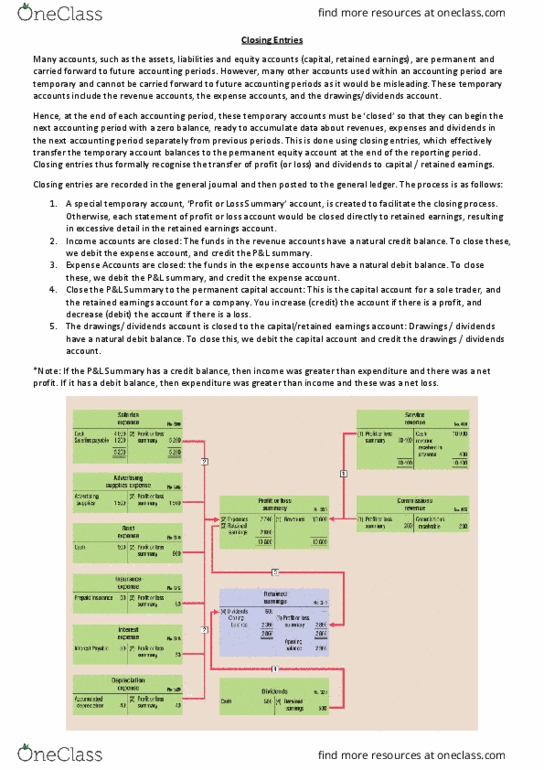

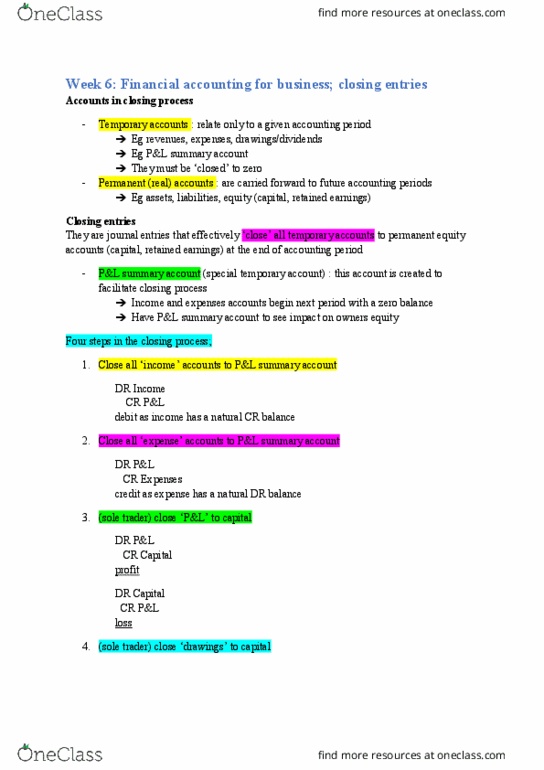

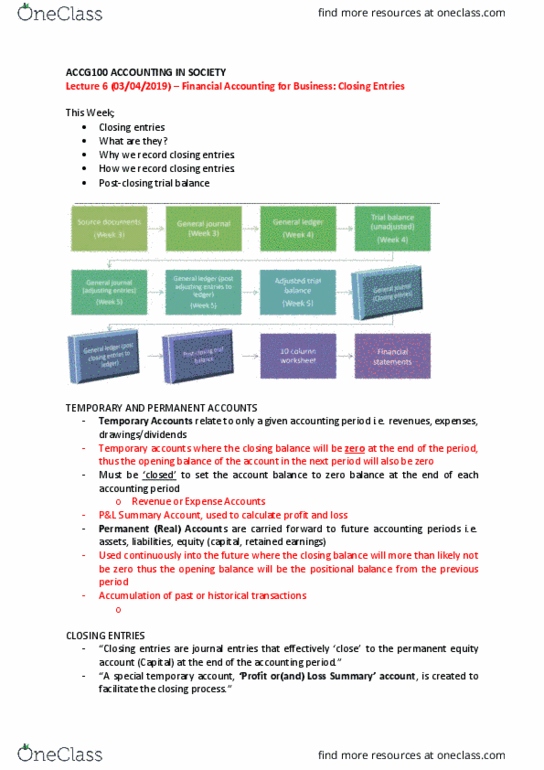

Once adjusting entries have been made, adjustments are posted to the individual general ledger accounts. The general ledger balances are then posted to the adjusted trial balance, which reflects all posted end-of-period adjusting entries. Temporary accounts relate to only a given accounting period i. e. revenues, expenses, drawings/dividends. Must be closed to set the account balance to zero balance at the end of each accounting period. Permanent (real) accounts are carried forward to future accounting periods. Journal entries that close all temporary accounts to the permanent equity account (capital) and the end of the accounting period. A special temporary account, profit or (and) loss summary account, is created to facilitate the closing process. Income and expense accounts then begin the next accounting period with a zero balance. Close all income accounts ( zero balance) to the p & l summary account.