ACCG100 Lecture Notes - Lecture 8: Current Liability, Profit Margin, Financial Statement

1 Sep 2018

School

Department

Course

Professor

Week 8: Financial accounting for business; interpreting financial

statements

Why analyse financial statements?

- Money $$ is important but useless when viewed in isolation

➔ Eg $20000 profit – is this good or bad?

▪ The answer depends on what you compare it to

- Relationships between items in the financial statements are important – making

comparison

Analysing financial statements

- Ratio analysis

➔ A ratio is a mathematical relationship between two different quantities

➔ Can be used to show relationships among items of financial data

➔ Expressed in terms of percentages, rates or proportions

➔ Interpreting ratios = need to compare

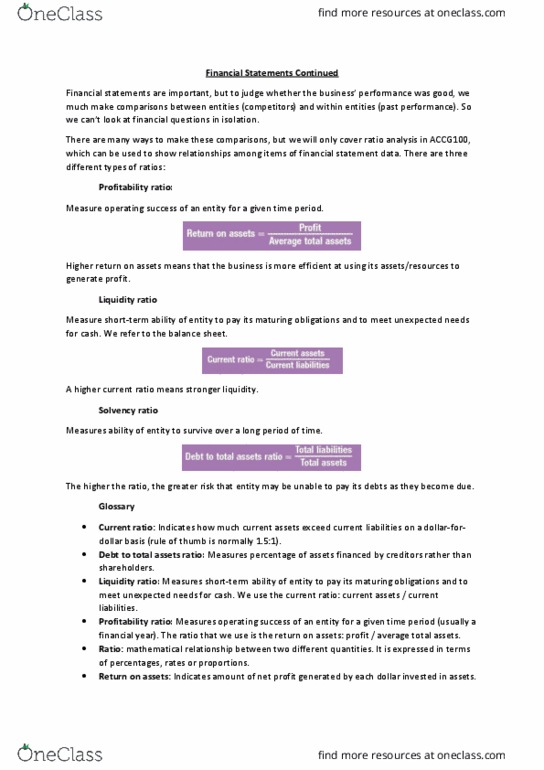

- 3 different types of ratios;

➔ Profitability ratio

▪ Return on assets

▪ Profit margin

➔ Liquidity ratio

▪ Current ratio

➔ Solvency ratio

▪ Debt to total assets ratio

Profitability ratio

- Measure operating success of an entity for a given time period

- Profit comes from P&L

➔ Return on assets : indicates amount of net profit generated by each dollar

invested in assets

➔ Profit margin : indicates amount of net profit generated by each dollar of sales

profit

Return on assets = average of total assets

profit

Profit margin = net sales

Document Summary

Week 8: financial accounting for business; interpreting financial statements. Money 24506 is important but useless when viewed in isolation. Eg profit is this good or bad: the answer depends on what you compare it to. Relationships between items in the financial statements are important making comparison. A ratio is a mathematical relationship between two different quantities. Can be used to show relationships among items of financial data. Expressed in terms of percentages, rates or proportions. Profitability ratio: return on assets, profit margin. Solvency ratio: debt to total assets ratio. Measure operating success of an entity for a given time period. Return on assets : indicates amount of net profit generated by each dollar invested in assets profit. Return on assets = average of total assets. Profit margin : indicates amount of net profit generated by each dollar of sales profit. Measures short-term ability of entity to pay its maturing obligations and to meet unexpected needs for cash.