ACCT10003 Lecture Notes - Lecture 9: Operating System, Engagement Letter, Internal Audit

19 Jun 2018

School

Department

Course

Professor

Accounting Processes and Analysis

Lecture 9: Internal Assurance

Auditing and Assurance

Assurance- The auditor’s ability to provide a degree of satisfaction regarding the reliability of the

information provided. The degree of satisfaction achieved is determined by the nature and extent of

procedures performed by the auditor, the results of the procedures and the objectivity of the evidence

obtained.

Assurance can be measured by:

degree of satisfaction

reliability of information

nature and extent of procedures

results of the procedures

objectivity of evidence

Accounting Processes and Financial Reports

Assertions made by Management

Existence or Occurrence- event reported is true

Completeness- nothing missing

Cut-off- asserting the sales correctly belong in the reporting period

Rights and obligations

Accuracy, classification, valuation and allocation

How do we have trust in the financial statements and how do we trust these assertions?

There will be external auditor’s reports attached to the financial reports, so see if they are in accordance

with accounting standards and corporations law. These reports are given to external users and give them

confidence in whether the reports have been prepared appropriately.

Key aspects of the external audit include:

Primary Objective: Enhance degree of confidence in financial statements by expressing opinion on

whether presented fairly

Applicable Professional Standards: IAASB including ISAs

Reporting Line: To owners

Reporting Format: Specified in ISA 700

Skills and Competence: Application of reporting and auditing standards

Engagement Terms: Engagement letter with management

Engagement Scope: Procedures to obtain evidence on financial statements (set in Auditing

standards and Corp. Act)

Evidence and Documentation: ISA 230 and 500

Employment and Remuneration: Organisation pays external audit firm which employs audit team.

find more resources at oneclass.com

find more resources at oneclass.com

Corporate Governance and Internal Controls

A set of processes and policies in managing an organization with sound ethics to safeguard the interests of

its stakeholders. It promotes accountability, fairness, and transparency in the organisation’s relationship

with its stakeholders.

Internal control needs to be a part of a firm’s governance structure. It includes the policies, systems and

procedures put in place to aid an organisation in managing its risk exposure and achieving its objectives.

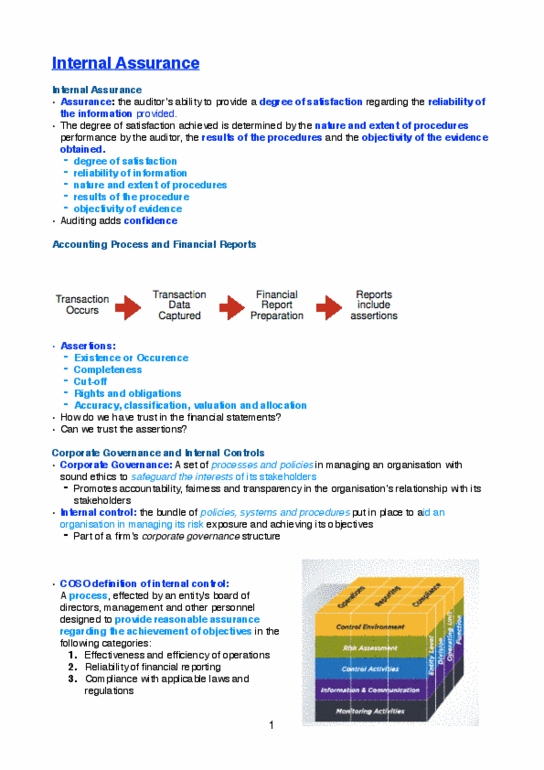

COSO Definition of Internal Control

A process, effected by an entity’s board of directors, management and other personnel, designed to provide

reasonable assurance regarding the achievement of objectives in the following categories:

Effectiveness and efficiency of operations

Effectiveness (doing the right things) and efficiency (doing the right things right) of operations

– Is the operational process meeting its process goals?

– Is the operational process meeting organisational goals?

– Are resources used/generated within a process used efficiently? Protected?

– OPERATIONALLY DRIVEN

Reliability of financial reporting

Reliability of reporting

– Financial statements– True & Fair view, Free of material misstatements

– Other reports

– INFORMATION DRIVEN

Compliance with applicable laws and regulations

Compliance with applicable laws and regulations

– Corporations Act

– Privacy Act

– Trade Practices Act

– Potentially several laws and regulations that could impact on an organisation’s

operations.

– COMPLIANCE DRIVEN

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Assurance- the auditor"s ability to provide a degree of satisfaction regarding the reliability of the information provided. The degree of satisfaction achieved is determined by the nature and extent of procedures performed by the auditor, the results of the procedures and the objectivity of the evidence obtained. Assurance can be measured by: degree of satisfaction reliability of information nature and extent of procedures results of the procedures objectivity of evidence. Cut-off- asserting the sales correctly belong in the reporting period. There will be external auditor"s reports attached to the financial reports, so see if they are in accordance with accounting standards and corporations law. These reports are given to external users and give them confidence in whether the reports have been prepared appropriately. Primary objective: enhance degree of confidence in financial statements by expressing opinion on whether presented fairly. Skills and competence: application of reporting and auditing standards.