ACC1200 Lecture Notes - Lecture 5: Cash Flow, Financial Statement, Income Statement

22 May 2018

School

Department

Course

Professor

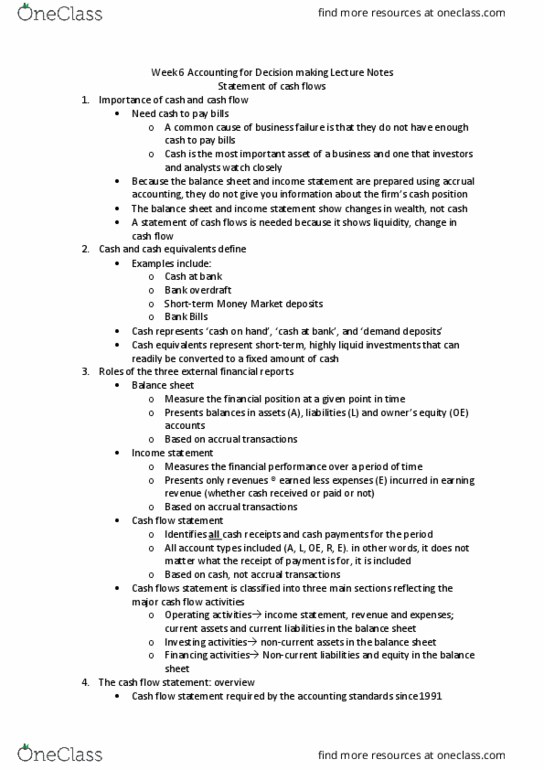

Week 5: Statement of Cash Flow

RECAP:

General Purpose financial statements: used to meet the needs of common information for external

users to assist them in decision making

• Balance sheet: wealth of entity at the point in time

o A, L, OE

• Statement of changes in equity: how the owner's wealth has changed during a financial period,

reconciles the OE value at the start and the end

• Income statement: shows the income performance, shows profit or the loss

• Statement of cash flows: focusses on activities only based on cash

Statement of cash flows

Shows activities and transactions that have been transacted in cash.

Profit vs Cash

• Profit: Recognizes the income when it earned and expense when it is incurred, regardless of

whether cash is received or paid at that time. It recognises accrual accounting methods.

• Cash: Based upon exchanges of cash only, provides details on where cash came from and

where it was spent on.

Importance of cash flow in a business

If they are unable to pay their employees, creditors etc, then they will be forced into bankruptcy,

liquidate assets to pay back debt or lose the opportunity of purchasing on credit.

Businesses can do the following to prevent the lack of cash:

• Follow good business practices (customer credit policies)

• Prepare a cash flow forecast or cash budget: an estimate of the cash coming and going out of

the business, helps to identify possible future cash shortages and allows the time needed to

take corrective action

Definition of cash

All cash, cash on hand and cash equivalents, for example

• Notes and coins

• Deposit call accounts at financial institutions

• Cash equivalents

• Short term, highly liquid investments easily converted to known amounts of cash with little

risk of a change in value

o Investments with maturity of less than 3 months

o Bank overdrafts

find more resources at oneclass.com

find more resources at oneclass.com

Types of cash flows:

1. Operational cash flows: cash received or spent as a result of a company's business activities

a. Payment to creditors

b. Cash received

2. Investment cash flows: cash received or spent through investing activities

a. Purchasing and selling of assets

3. Financing cash flows: cash received or paid out as debt through repayments

a. Loans

b. Payments to pay debts

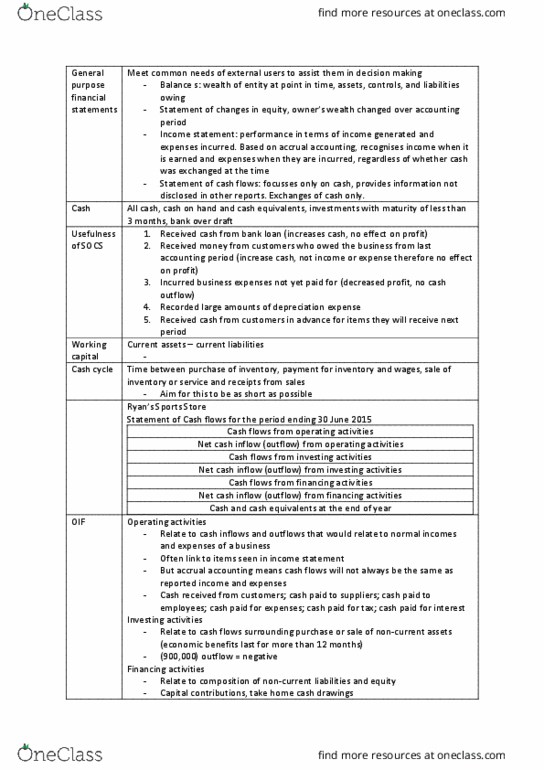

Working Capital = current assets - current liabilities

Cash cycle

Format for the statement of cash flows

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

General purpose financial statements: used to meet the needs of common information for external users to assist them in decision making: balance sheet: wealth of entity at the point in time, a, l, oe. Statement of changes in equity: how the owner"s wealth has changed during a financial period, reconciles the oe value at the start and the end. Income statement: shows the income performance, shows profit or the loss. Statement of cash flows: focusses on activities only based on cash. Shows activities and transactions that have been transacted in cash. Profit vs cash: profit: recognizes the income when it earned and expense when it is incurred, regardless of whether cash is received or paid at that time. It recognises accrual accounting methods: cash: based upon exchanges of cash only, provides details on where cash came from and where it was spent on.