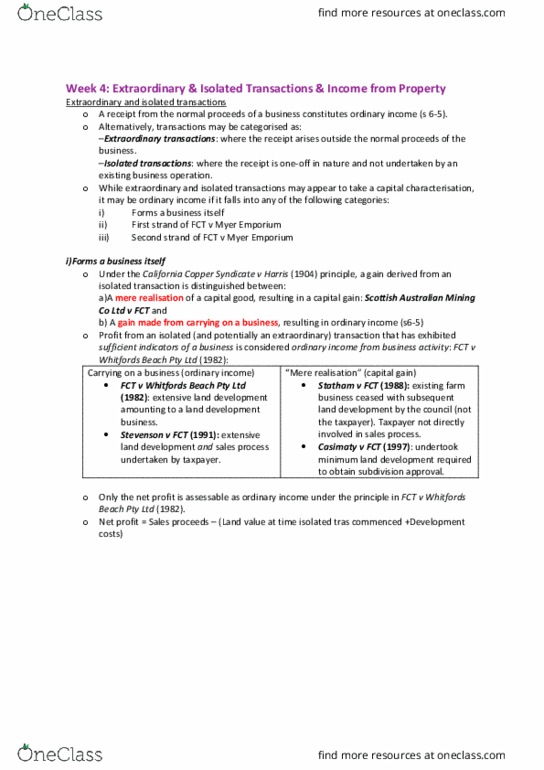

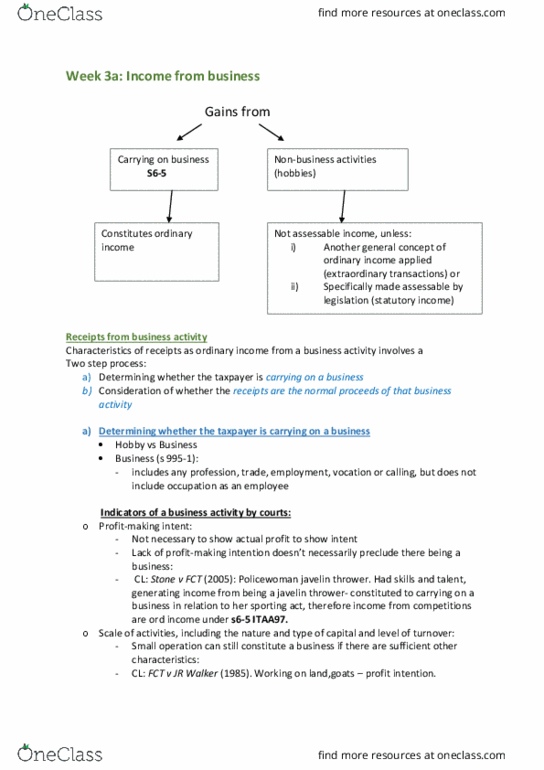

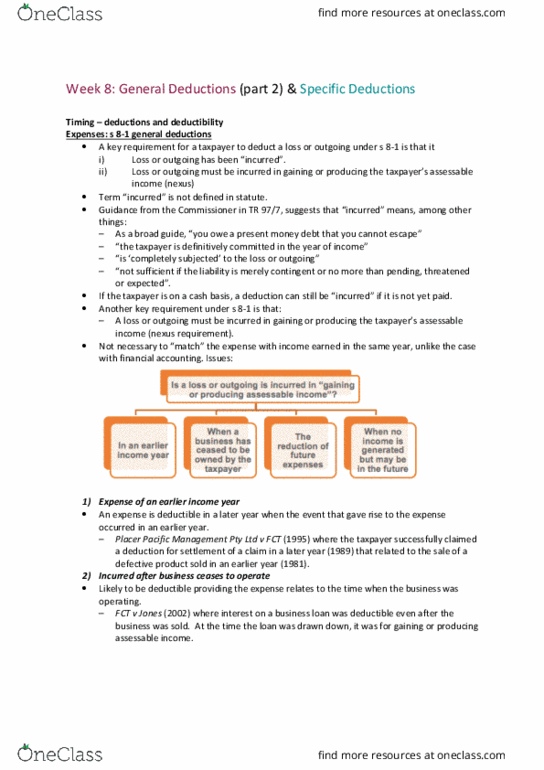

BTC3150 Lecture Notes - Lecture 4: Bitcoin, Capital Expenditure, 6 Years

!

Week!6:!Capital!Gains!Tax!

!

•A!gain!characterised!as!capital!is!not!subject!to!income!tax!under!ordinary!concepts.!

•Capital!gains!tax!(CGT)!commenced!on!20!September!1985!and!brings!capital!receipts!into!the!tax!

base.!

•A!taxpayer’s!income!tax!liability!includes!a!net!capital!gain:!!

!

!

!

CGT$effects$on$taxpayer$

• Ultimately,!a!“net!capital!gain”!is!included!in!the!taxpayer’s!assessable!income.!

• Liability!to!CGT!is!determined!by!following!the!process:!

!!!!!! !

!

Step$1:$Capital$gain$or$a$capital$loss?$

• To!determine!whether!the!taxpayer!has!made!a!capital!gain!or!capital!loss,!the!following!

issues!are!considered:!

!!!! !

1. CGT$Event$

• A!taxpayer!only!makes!a!capital!gain!or!loss!if!a!CGT!event!occurs:!s!102-20.!

• Sometimes,!more!than!one!CGT!event!will!happen.!!Generally,!the!most!specific!to!the!

situation!is!used:!s!102-25(1).!

• 52!CGT!events!exist.!For!summary!of!CGT!events,!see!s!104-5.!

• The!following!key!CGT!events!are!covered!in!these!slides:!

–CGT!event!A1!–!Disposals!

–CGT!event!C1!and!C2!–!End!of!a!CGT!asset!

!!!!!!!!!!!!!!!–CGT!event!D1!–!Bringing!into!existence!a!CGT!asset!

!

!

!

Assessable!Income!=!Ordinary!Income!+!Statutory!Income!(NET!CAPITAL!GAIN)!

!

a)CGT$Event$A1$–$Disposal$(s$104-10(1))$

• Occurs!when!the!taxpayer!disposes!of!a!CGT!asset.!

• Time!of!the!CGT!event:!

–When!the!taxpayer!enters!into!the!contract,!or!

–If!no!contract,!when!ownership!change!occurs.!!See,!FCT$v$Sara$Lee$Household.!

• Timing!of!CGT!event!(and!hence!capital!gain!or!loss)!will!be!in!the!income!year!ended!30!

June!X1$

$

!!!!!!!!!!!!!!! !

• Under!CGT!event!A1,!!

Capital!gain!=!Capital!proceeds!–!Cost!base!

Capital!loss=!!Reduced!cost!base!–!Capital!proceeds!

b)CGT$event$C1$-$End$of$a$CGT$asset$(s$104-20(1))$

• Occurs!if!a!CGT!asset!that!the!taxpayer!owns!is!lost!or!destroyed.!

• Time!of!the!CGT!event:!when!the!taxpayer!first!receives!compensation!for!the!loss!or!

destruction,!or!if!no!compensation,!when!the!loss!is!discovered!or!the!destruction!occurred.!

c)CGT$event$C2$-$End$of$an$intangible$asset$(s$104-25(1))$

• Occurs!if,!broadly,!ownership!of!the!taxpayer’s!intangible!asset!ends!by,!among!other!things,!

cancellation!or!expiration.!

• Time!of!the!CGT!event:!when!the!taxpayer!enters!into!the!contract!that!results!in!the!asset!

ending.!

d)CGT$event$D1$-$Asset$into$existence$(s$104-35(1))$

• Occurs!where!a!taxpayer!creates!a!contractual!or!other!legal!right!in!another!entity,!for!

example:!

– Restraint!of!trade!where!a!taxpayer!agrees!not!to!operate!a!similar!business!within!a!

particular!radius.!

– Exclusive!trade!agreements.!

• Time!of!the!CGT!event:!when!the!taxpayer!enters!into!the!contract!or!creates!the!right.!

e) CGT$event$I1$–$End$of$Australian$residency$(s$104-160(1))!

• Occurs!when!a!taxpayer!stops!being!an!Australian!resident!

– Taxpayer!may!elect!to!disregard!the!capital!gain/loss!

– Assets!deemed!to!be!taxable!Australian!property!until!a!CGT!event!happens!or!the!

taxpayer!becomes!an!Australian!resident.!

f)CGT$event$I2$–$Trust$stops$being$a$resident$trust$(s$104-170(1))!

• Occurs!when!a!trust!stops!being!a!resident!trust!for!CGT!purposes.!

!

2.$$CGT$Asset!

• Broad!definition!of!a!CGT!asset.!!Defined!in!s!108-5(1)!as:!

–Any!kind!or!property;!or!

–Legal!or!equitable!right!that!is!not!property.!

• Examples!include:!!

–Land!and!buildings!

–Shares!in!a!company!/!units!in!a!unit!trust!

–Collectibles!costing!over!$500!(eg!stamp!collection)!

–Personal!use!assets!costing!over!$10,000!(eg!boat)!

–Contractual!rights!(eg!restraint!of!trade)!

–Business!goodwill.!

!!!!!!!•Commissioner!has!suggested!bitcoin!is!a!CGT!asset.!

!

!

!

!!!!!!!!!!!! !

!

a) Collectibles$

o Defined!in!s!108-10(2)!as:!

– Artwork,!jewellery,!an!antique!or!a!coin!or!medallion;!or!

– A!rare!folio,!manuscript!or!book;!or!

– A!postage!stamp!or!first!day!cover;!

o That!is!used!or!kept!mainly!for!personal!use!or!enjoyment!

o Age>100!years.!Eg!engine!sports!car!(No!CGT!on!cars-exempt,!even!if!vintage)!

!

Special!rules!apply!to!collectibles:!

!

b) Personal$use$assets$

o Defined!as!an!asset!(other!than!a!collectible)!that!is!used!or!kept!mainly!for!personal!use!or!

enjoyment,!excluding!land!or!buildings!(s!108-20(2)).!

o Examples!include:!

–Television!at!home!

–Mobile!telephone!for!private!use!

–A!bicycle!

–A!yacht!owned!for!personal!use!and!enjoyment.!

o Does!not!include!land!or!building,!or!if!considered!a!collectible!(s!108-20(3)).!

!!!!!!!!!!Special!rules!apply:!

Document Summary

Assessable income = ordinary income + statutory income (net capital gain) Cgt effects on taxpayer: ultimately, a net capital gain is included in the taxpayer"s assessable income. Liability to cgt is determined by following the process: Sometimes, more than one cgt event will happen. Generally, the most specific to the situation is used: s 102-25(1): 52 cgt events exist. For summary of cgt events, see s 104-5: the following key cgt events are covered in these slides: Cgt event c1 and c2 end of a cgt asset. Cgt event d1 bringing into existence a cgt asset a)cgt event a1 disposal (s 104-10(1): occurs when the taxpayer disposes of a cgt asset, time of the cgt event: When the taxpayer enters into the contract, or. See, fct v sara lee household: timing of cgt event (and hence capital gain or loss) will be in the income year ended 30. Capital gain = capital proceeds cost base.