ACCT10003 Lecture 9: Internal Assurance - Lecture 9

17 May 2018

School

Department

Course

Professor

Internal Assurance

Internal Assurance

•Assurance: the auditor’s ability to provide a degree of satisfaction regarding the reliability of

the information provided.

•The degree of satisfaction achieved is determined by the nature and extent of procedures

performance by the auditor, the results of the procedures and the objectivity of the evidence

obtained.

-degree of satisfaction

-reliability of information

-nature and extent of procedures

-results of the procedure

-objectivity of evidence

•Auditing adds confidence

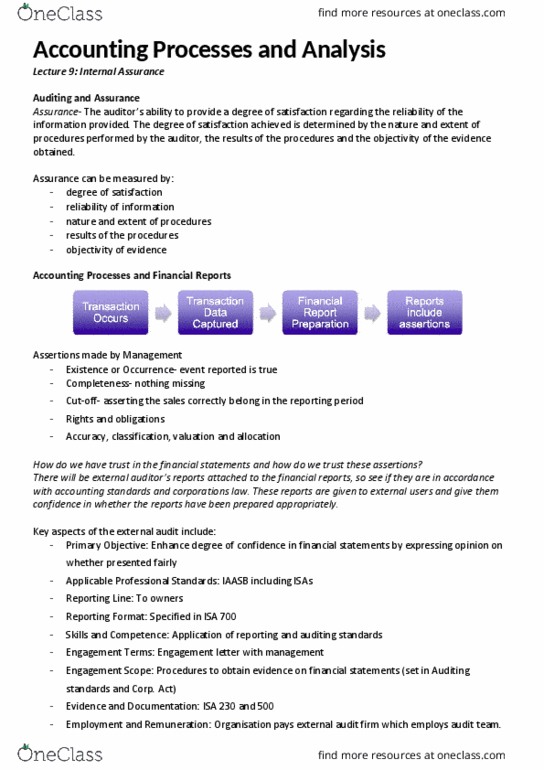

Accounting Process and Financial Reports

•Assertions:

-Existence or Occurence

-Completeness

-Cut-off

-Rights and obligations

-Accuracy, classification, valuation and allocation

•How do we have trust in the financial statements?

•Can we trust the assertions?

Corporate Governance and Internal Controls

•Corporate Governance: A set of processes and policies in managing an organisation with

sound ethics to safeguard the interests of its stakeholders

-Promotes accountability, fairness and transparency in the organisation’s relationship with its

stakeholders

•Internal control: the bundle of policies, systems and procedures put in place to aid an

organisation in managing its risk exposure and achieving its objectives

-Part of a firm’s corporate governance structure

•COSO definition of internal control: !

A process, effected by an entity's board of

directors, management and other personnel

designed to provide reasonable assurance

regarding the achievement of objectives in the

following categories:

1. Effectiveness and efficiency of operations

2. Reliability of financial reporting

3. Compliance with applicable laws and

regulations

1