FINS3630 Lecture Notes - Lecture 5: Interest Rate Risk, Canons Regular, Reinvestment Risk

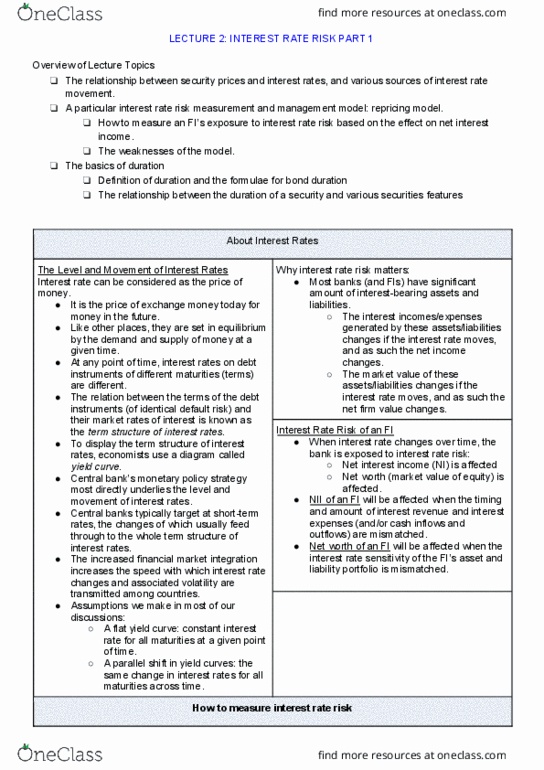

Lecture 2: Interest rate risk

- FI perform maturity intermediation between households and firms → LT IR fixed vs.

deposit IR (rolled over) vary w market IR

- Measure of effets of IR ∆: Net interest income (interest income – interest expenses) →

repricing model (rollover of asset or variable rate instrument)

o Net worth: MV A – MV L → duration model

- Central banks influence ST rates (but this transfers to LT rates)

- Rate sensitive A/L (RSA/RSL- repriced w/in maturity bucket)

o Maturity buckets: 1 day, >1d-3m, >3m-6m, >6m-1y, >1y-5y, >5y

o Reasons for repricing: rollover of A, variable rate instrument

o Repricing GAP(i) = RSA(i) – RSL(i)

▪ When negative: RSA<RSL in bucket I → -ve GAP esp CGAP exposes FI to

refinancing risk

▪ Positive exposes FI to reinvestment risk

o Cuulatie CRSA = ∑RSA or L

o Cuulatie repriig gap: CGAP = ∑GAP

o ∆NII = GAPi ∆Ri

o ∆CNII = ∑∆NII

o gap ratio: CGAP(i)/Assets → standardise

o assue ∆rRSA ≠ ∆rRSL ie spread effet

▪ ∆NII = RSA*∆rRSA – RSL*∆rRSL at i

▪ ∆CNII = CRSA*∆rRSA – CRSL*∆rRSL at i

- weakness of repricing model: 21-25

o run-off problem

o ignorance of OBS activities

o ignores distribution of A/L w/in maturity bucket and over-aggregation

o does not consider MV effects

find more resources at oneclass.com

find more resources at oneclass.com

- duration

o duration depends purely on how its price is determined by IR → sesitiit of MV ∆

of the fiaial istruet to a ∆ i IR IR elastiit

o

o macaulay duration:

o modified duration: mD = D/1+r

o dollar duration: DD = MD*P

o zero coupon bonds: sell at the deepest discount (CPN rate cannot go below zero)

o higher cpn = lower duration

Interest rate risk II

- coupons = lower duration (receive PV of CF earlier)

- duration increases maturity

-

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Fi perform maturity intermediation between households and firms lt ir fixed vs. deposit ir (rolled over) vary w market ir. Measure of effe(cid:272)ts of ir : net interest income (interest income interest expenses) repricing model (rollover of asset or variable rate instrument: net worth: mv a mv l duration model. Central banks influence st rates (but this transfers to lt rates) Weakness of repricing model: 21-25: run-off problem ignorance of obs activities ignores distribution of a/l w/in maturity bucket and over-aggregation, does not consider mv effects. Interest rate risk ii coupons = lower duration (receive pv of cf earlier) Duration of annuity: duration of annuity does not matter on cf, is influenced by rates and pattern of cf consul bond = perpetuity. Duration: degree to which changes in interest rates change of value of asset immunisation: d(a) = d(l) = wx*dx + wy*dy.