ECON 1P91 Lecture Notes - Lecture 7: Deadweight Loss, Allocative Efficiency, Longrun

20 May 2016

School

Department

Course

Professor

19

ECON 1P91 Full Course Notes

Verified Note

19 documents

Document Summary

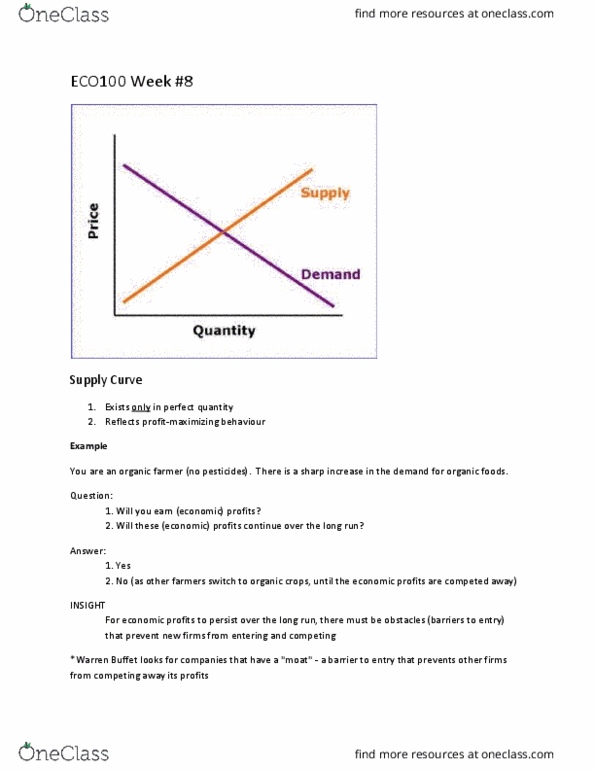

Where tr is just enough to cover tvc (all variable costs) Only fixe costs remain (economic costs= fixed costs) Even with zero output, still have fixed costs. Firm indifferent at this point can produce or shut down. If price falls below the minimum average variable costs, the firm will shut down (p< min avc) Short run supply curve is marginal cost curve at and above minimum point of average variable cost curve. Q=2200 q # firms = q (a) industry or market (b) firm. At q, find atc economic profit (p-ac)q (a) All costs identical in the long run long-run market supply is horizontal. Long-run average cost curve (lrac)is at capacity. Value consumers place on a good minus price paid for it. Measured by area between demand curve and price paid. Enter until economic profit = zero (normal profits) Innovation and technological change can create substitutes and weaken existing monopolies. They serve to protect the firm from competition.