COMM 1102 Lecture Notes - Lecture 12: Fixed Cost

15 Oct 2018

School

Department

Course

Professor

Document Summary

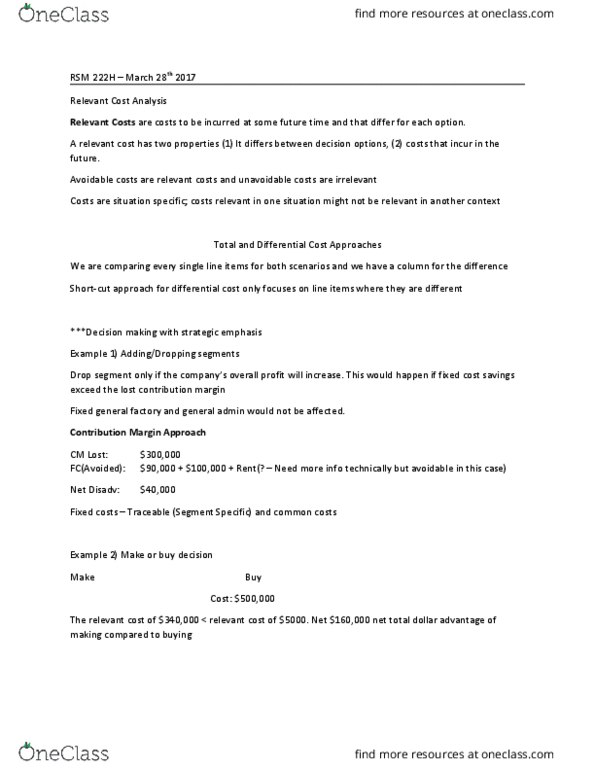

Deal with circumstances that are rare for a company to face - and should only be used in the rare situations. A relevant cost: a cost that differs between alternatives. An avoidable cost: a cost that can be eliminated by choosing one alternative over another. Costs that are never relevant are: sunk costs, future costs. We don"t use them in our analysis because they are irrelevant. *pick relevant costs and ignore the irrelevant costs. We allocate/assign traceable and variable costs but not common costs. A company should drop a segment only if profits would increase. This would only happen if the fixed cost savings exceed the lost contribution margin. Salaries of manager, rent on factory, and advertising - all relevant costs. The company allocated common fixed costs to the segment, which made it appear to be less profitable - this can be misleading. When a company is invalid in more than one activity in the entire value chain.