COMM 2202 Lecture Notes - Lecture 2: Capital Cost Allowance, Capital Asset, Retained Earnings

13 Dec 2018

School

Department

Course

Professor

Document Summary

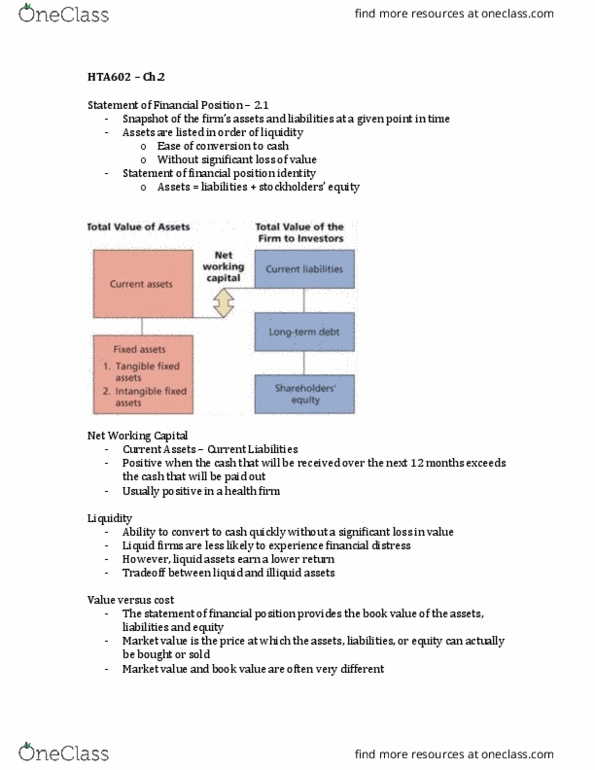

Chapter 2: financial statements, taxes and cash flow. Cca (capital cost allowance) - depreciation for tax purposes. Capital structure (long term debt + shareholders" equity) Net working capital = current assets current liabilities. Positive when cash received exceeds cash to be paid out. Liquidity: ease of conversion to cash without signi cant loss of value: liquid rms are less likely to experience nancial distress, liquid assets learn a lower return, tradeoff between liquid and illiquid assets. Book value and market value of debt tends to not uctuate as much as assets and equity. Matching principle - main reason the net income and cash ow differ. Sales, cogs, interest and taxes are cash ows. Net income is owned by shareholders - residual earners. It can either go back to the company in retained earnings or payed out to shareholders as dividends.