COMM 2202 Lecture Notes - Lecture 13: Squared Deviations From The Mean, Expected Return, Standard Deviation

13 Dec 2018

School

Department

Course

Professor

Document Summary

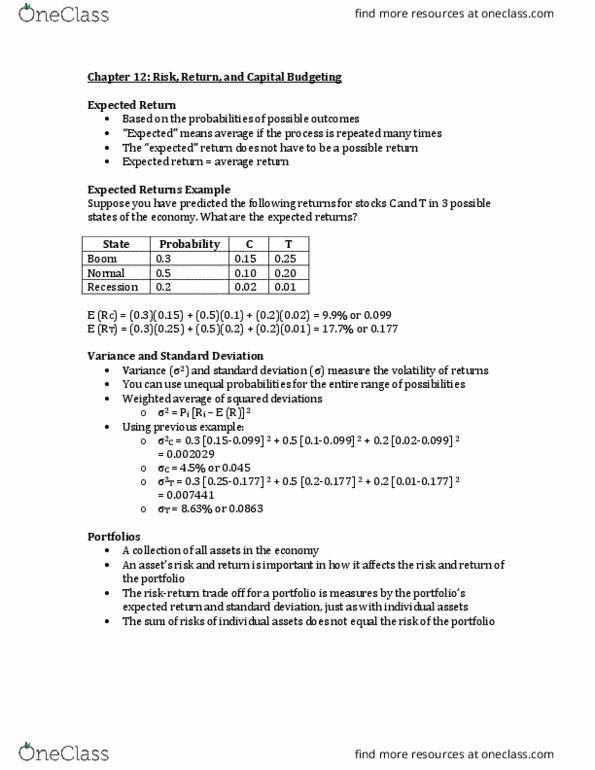

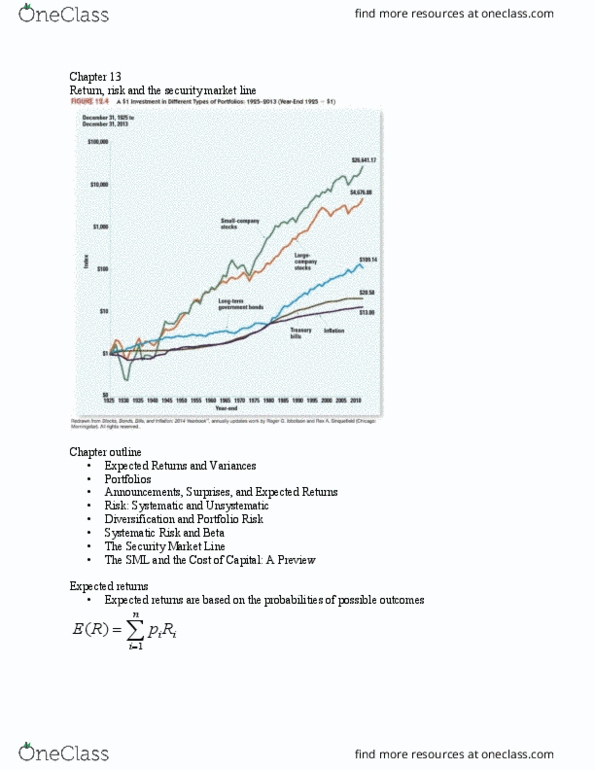

Chapter 13: return, risk, and the security market line. Expected returns: expected returns are based on the probabilities of possible outcomes, in this context, expected means average if the process is repeated many times, the expected return does not even have to be a possible return. The sum of the probabilities multiplied by the expected return. Suppose you have predicted the following returns for stocks c and t in three possible states of nature. Return (c) = . 3(. 15) + . 5(. 10) + . 2(. 02) = . 099 = 9. 9% = expected return. Return (t) = . 3(. 25) + . 5(. 20) + . 2(. 01) = . 177 = 17. 7% Generally, the better the economy, the better the return on the stocks. Variance and standard deviation: variance and standard deviation still measure the volatility of returns or measure of risk, you can use unequal probabilities for the entire range of possibilities, weighted average of squared deviations.