CCFC 513 Lecture Notes - Lecture 4: Retained Earnings, Consolidated Financial Statement, Equity Method

25 Jun 2018

School

Department

Course

Professor

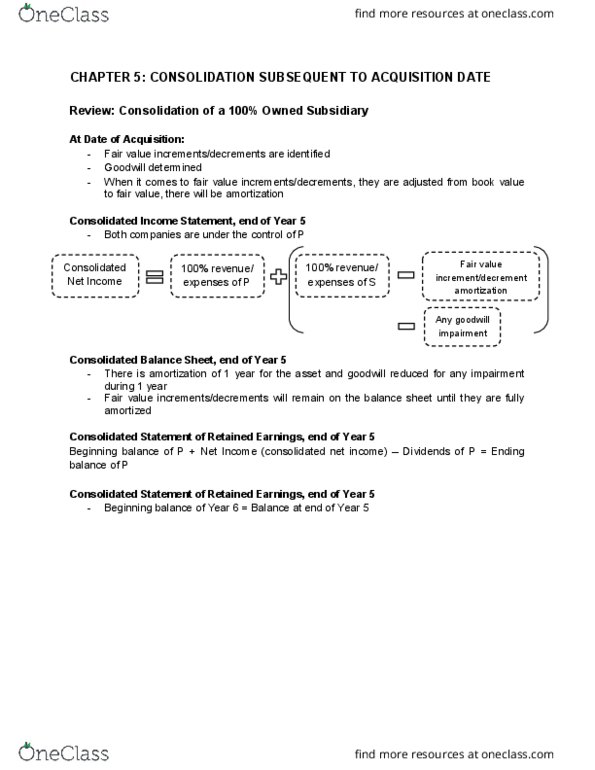

CHAPTER 5: CONSOLIDATION SUBSEQUENT TO ACQUISITION DATE

Scenario 1: Buy net assets

Scenario 2: Buy shares

- Use equity method or cost method

- Make consolidated financial statement

What happens after date of acquisition? (Make reference to a building on the books of S)

- In Scenario 1, the title of building gets transferred to the parent and recorded in the

parent’s book at fair value

- In Scenario 2, it was a transaction between the parent and the shareholders so the

assets (i.e. building) did not change; subsidiary’s books remain unchanged

Rule #1: All fair value increments and decrements (e.g. adjustments) need to be amortized

- Inventory: the fair value increments/decrements of inventory would be amortized over

the remaining life of the inventory

- Same applies for all other assets or liabilities on the balance sheet

Effect of amortization on income statement

Assets (DR on balance sheet)

- The amortization of an asset will be a DR on the income statement because it is an

expense

- Example: Building amortization

Depreciation expense

100,000

Accumulated depreciation

100,000

Liabilities

- The amortization of liability will be a CR on the income statement

- Example: fair value decrements of a liability

Liability

100,000

Expense

100,000

5.1 Consolidation of a 100% Owned Subsidiary

Example 1: P purchased 100% of the outstanding common shares of S for $19,000

- Which method should be used? Cost or equity method?

- Under cost method, when dividends are paid, the entry to record the dividend received is

as follows:

Cash

2,500

Dividend income

2,500

Document Summary

What happens after date of acquisition? (make reference to a building on the books of s) In scenario 1, the title of building gets transferred to the parent and recorded in the parent"s book at fair value. In scenario 2, it was a transaction between the parent and the shareholders so the assets (i. e. building) did not change; subsidiary"s books remain unchanged. Rule #1: all fair value increments and decrements (e. g. adjustments) need to be amortized. Inventory: the fair value increments/decrements of inventory would be amortized over the remaining life of the inventory. Same applies for all other assets or liabilities on the balance sheet. The amortization of an asset will be a dr on the income statement because it is an expense. The amortization of liability will be a cr on the income statement. Example: fair value decrements of a liability. Example 1: p purchased 100% of the outstanding common shares of s for ,000.