ECON 208 Lecture Notes - Root Mean Square, Marginal Product, Diminishing Returns

ECON 208 Full Course Notes

Document Summary

Get access

Related Documents

Related Questions

There are three types of barber shops in a competitive market in Seattle. Due to the peculiarities of zoning in Seattle, shop space can be rented in only three sizes: 1000 square feet, 2000 square feet, and 3000 square feet. For each of the three square footages, the information below shows the number of haircuts that can be sold as you increase the number of full-time barbers. The Barbers Union requires you to hire people full-time or not at all. (In other words, these are the only choices for workers and the barber shops.) For every 1000 square feet of space you rent, the annual rent is $40 per square foot and you must sign a one-year lease. The annual wage for a full-time barber is $30,000. These represent all economic costs including the normal profit.

| Number of Barbers (1000 Sq. Feet) | Number of Haircuts (1000 Sq. Feet) | Number of Barbers (2000 Sq. Feet) | Number of Haircuts (2000 Sq. Feet) | Number of Barbers (3000 Sq. Feet) | Number of Haircuts (3000 Sq. Feet) |

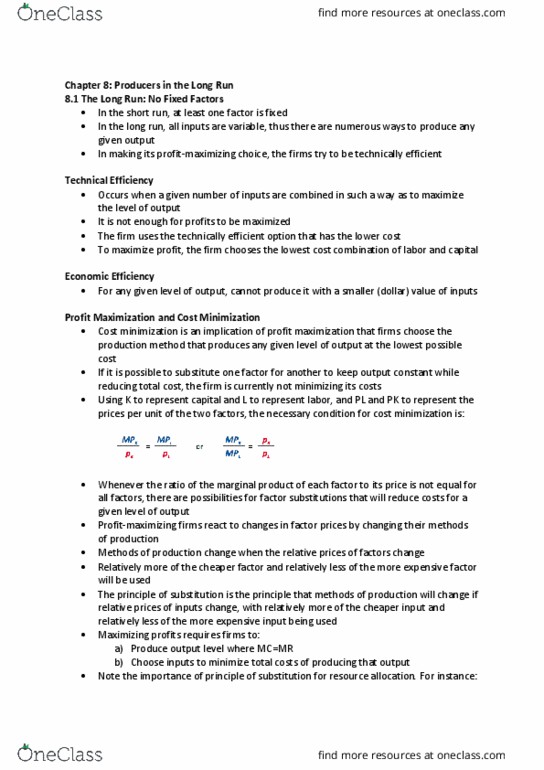

| 0 | 0 | 0 | 0 | 0 | 0 |

| 1 | 4000 | 1 | 4920 | 1 | 5560 |

| 2 | 6080 | 2 | 7480 | 2 | 7720 |

| 3 | 7720 | 3 | 9480 | 3 | 10520 |

| 4 | 8600 | 4 | 10520 | 4 | 12760 |

| 5 | 9320 | 5 | 11440 | 5 | 14640 |

| 6 | 9960 | 6 | 12240 | 6 | 16280 |

| 7 | 10520 | 7 | 12920 | 7 | 16400 |

Given the wage and rental information above, for each square footage what is the short-run average total cost of producing 10520 haircuts? [Remember that short-run average total cost includes both average variable and average fixed costs.] The long run average cost for a level of output is the lowest short run average total cost at which you can produce that output. What is the long-run average total cost of producing 10520 haircuts? Explain your choices.

For shops with each square footage, determine for each number of barbers listed, the total variable cost, total fixed cost, total cost, average variable cost, average total cost, average fixed cost, and marginal cost.

The leases for the year have all been signed and the market price is $18. What is the profit-maximizing number of barbers to hire for the shops at each square footage? What profits are earned in the barber shops with each square footage? Explain your choice.

Consider the long-run situation in the market where there is strong price competition, barbershops can change the square footage in their shop, and barber shops enter and exit the market. What do you anticipate will be the price in the long run? Based on that price, what will be the shops optimal choice of shop size and number of barbers in the shop in the long run? Explain your logic.