MGCR 211 Lecture Notes - Lecture 6: Weighted Arithmetic Mean, Uptodate

3 Sep 2016

School

Department

Course

Professor

Document Summary

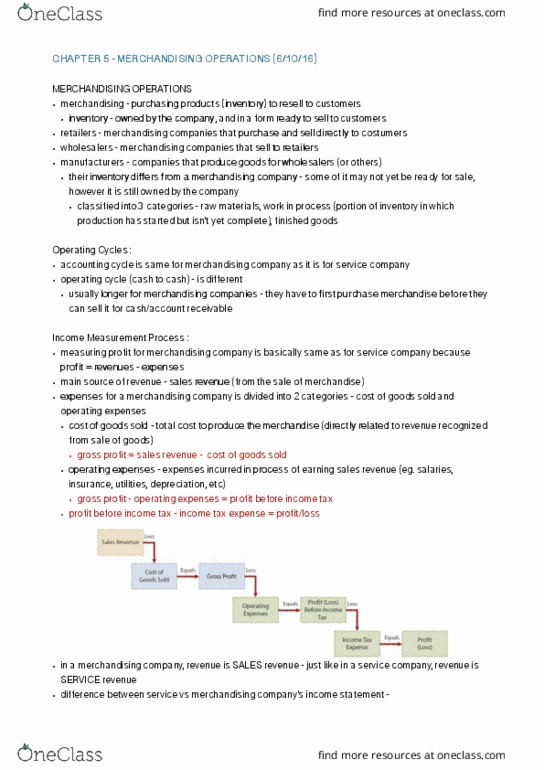

Any item purchased for resale or manufacturing of goods to be sold. Recorded at its cost on the date of acquisition. Income is recognized when the inventory is sold. Inventory appears on the balance sheet at lower of cost or net realizable value. A unit sold is immediately removed from the inventory account. Ending inventory and cost of goods sold are up-to-date. Better information (includes losses due to theft, damage etc) but at a higher cost. At the end of the period, inventory is counted and the cost of goods is calculated. First-in, first-out- the first item purchased is the first item sold. Weighted average- the cost of items is determined with a weighted average of items purchased.