MGCR 293 Lecture Notes - Lecture 3: Taipei Metro, Farad, Marginal Cost

13 Sep 2016

School

Department

Course

Professor

Document Summary

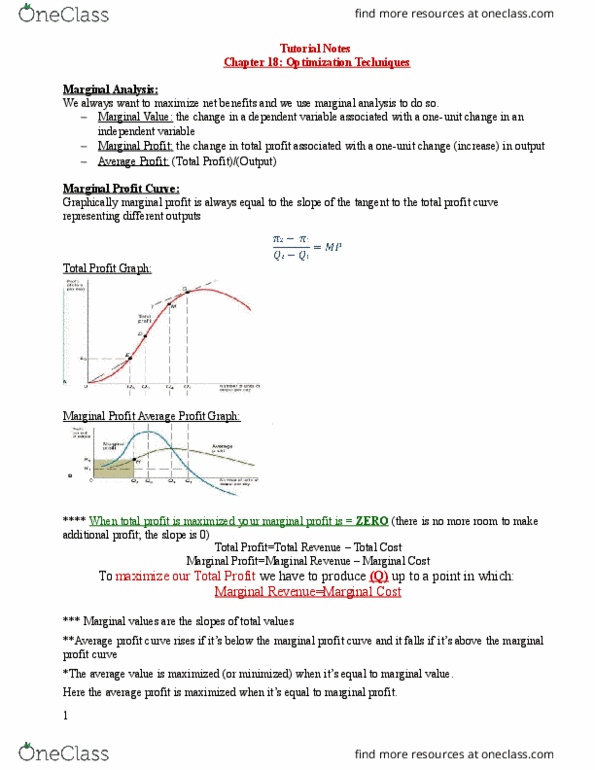

The number of units sold is a function of price. The marginal value of a dependent value is the change in this dependent variable (ex: associated with a 1-unit change in a particular independent variable (ex: p) Therefore marginal profit is the profit associated with one additional unit of output. Marginal cost is the cost associated with one additional unit of output. The dependant variable is maximized when its marginal value shifts from positive to negative. Positive and negative relationships: upward sloping= when x increases, y increases, supply, downward sloping= when x increases, y decreases, demand. When total profit is maximum, the slope of the total profit function is zero and marginal profit intersects the horizontal axis. Average profit curve rises if it is below the marginal profit curve and it falls if its is above the marginal profit curve. Average profit is maximized when it"s equal to marginal profit. Note: optimization refers to both maximumizing and minimizing.