MGCR 341 Lecture Notes - Lecture 7: Call Option, Risk-Free Interest Rate, Portfolio Insurance

16 Dec 2017

School

Department

Course

Professor

Document Summary

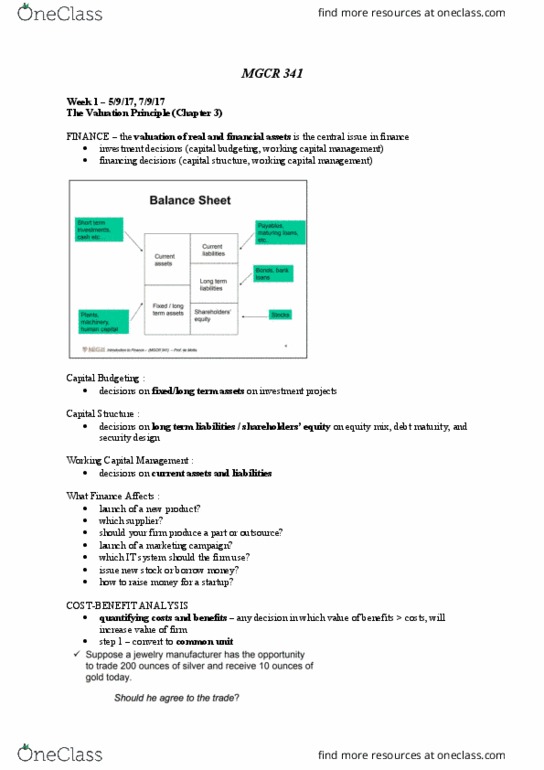

Option payoffs and profits at expiration to assess what an option is worth. The binomial option pricing model: making assumption that at the end of the next period the stock price has only 2 possible values. = # of shares of stock we purchase: b = investment in the risk-free asset (if b<0, means that rather than investing in the risk-free asset, the replicating portfolio requires borrowing b at the risk-free rate) 62 + 1. 05 b = 10 in down state , value must be sh : 42 + 1. 05 b = 0 ( 62 + 1. 05 b = 10) ( 42 + 1. 05 b = 0) = 20 = 10 subtracting down state from up state. C0 (call today) = value of replicating portfolio = value of 0. 5 shares amount borrowed = 0. 5x52-20 =6 thus price of call today = .