COMMERCE 1BA3 Lecture Notes - Matching Principle, Interest Rate, Deferral

2 Nov 2013

School

Department

Course

Professor

Document Summary

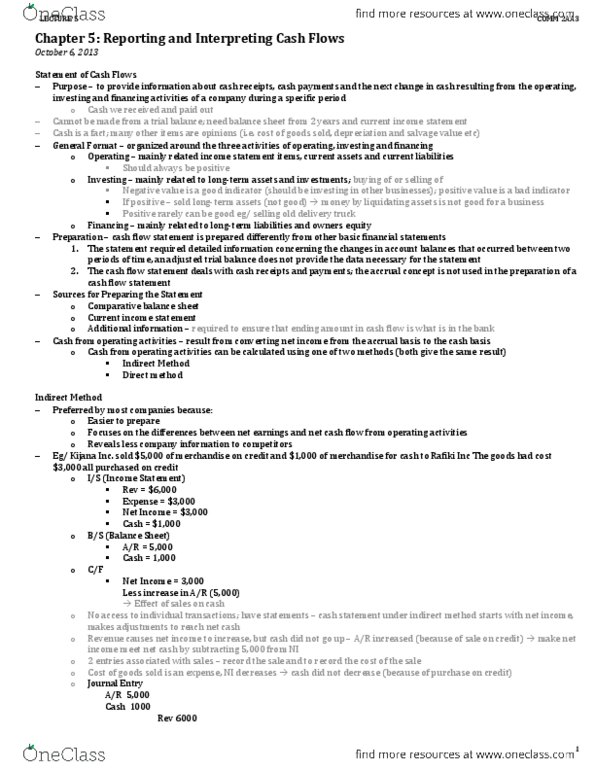

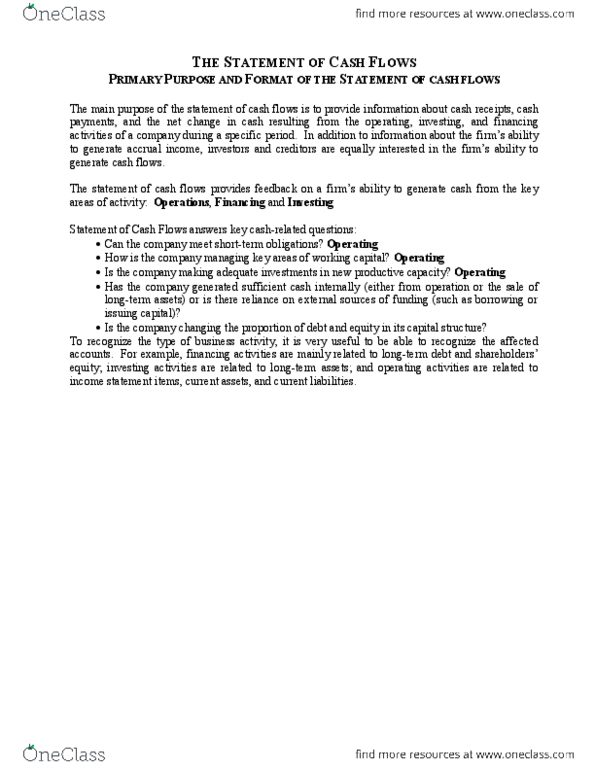

The purpose of the statement of cash flows. To provide information about: cash receipts, cash payments, net change in cash from the operating, investing, financing activities of a company during a specific period of time. Income statement, balance sheet, statement of changes in equity all require a trial balance to be made. Cash flow statement cannot be made using a trial balance. Cash flow statement is made using: balance sheet from last year, balance sheet from this year, income statement. Companies require a positive cash flow to keep running. Cash flow statement is divided into three sections: operating, mainly related to income items, current assets and current liabilities, ex. A/r, prepaid rent, a/p: expect operating expenses to be positive, calculates how long a business can go without shutting down, investing, mainly related to long-term assets and investments, purchase/sale of long-term assets and long-term investments, ex.