COMMERCE 1BA3 Lecture Notes - Perpetual Inventory, Inventory Turnover, Gross Margin

14 Jul 2014

School

Department

Course

Professor

Document Summary

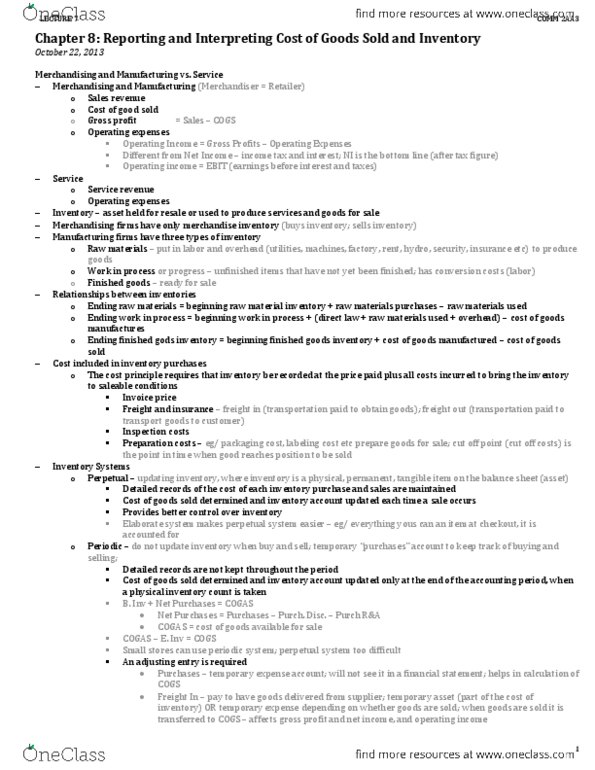

Objective 1: account for inventory using the perpetual and periodic inventory systems: the merchandising company"s balance sheet includes a new current asset, inventory or. Merchandise inventory. while the company"s income statement includes an expense, Cost of goods sold or cost of sales . Exhibit 6-1 contrasts the balance sheet and income statement of a service company versus a merchandiser. An item in your inventory had a cost of . When the above two entries are made to record the sale, what is the difference in the credit to revenue and the debit to cost of. , the amount of gross margin on the sale. The quantity and cost of the inventory on hand can be determined from inventory records, although an actual physical count must still be made at least once a year. Perpetual records give up-to-the-minute data about inventory, enabling managers to make decisions about when and how much to buy.