ECON 1B03 Lecture Notes - Lecture 5: Average Cost, Production Function, Average Variable Cost

9 Mar 2018

School

Department

Course

Professor

46

ECON 1B03 Full Course Notes

Verified Note

46 documents

Document Summary

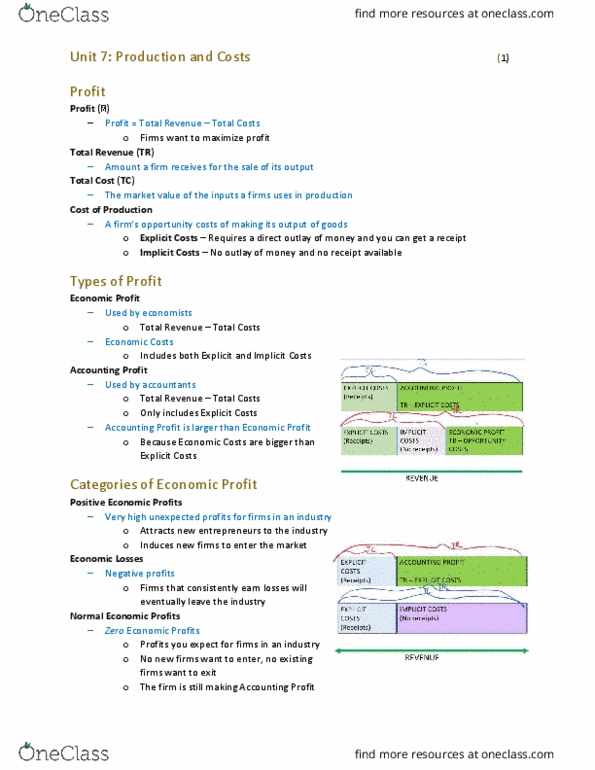

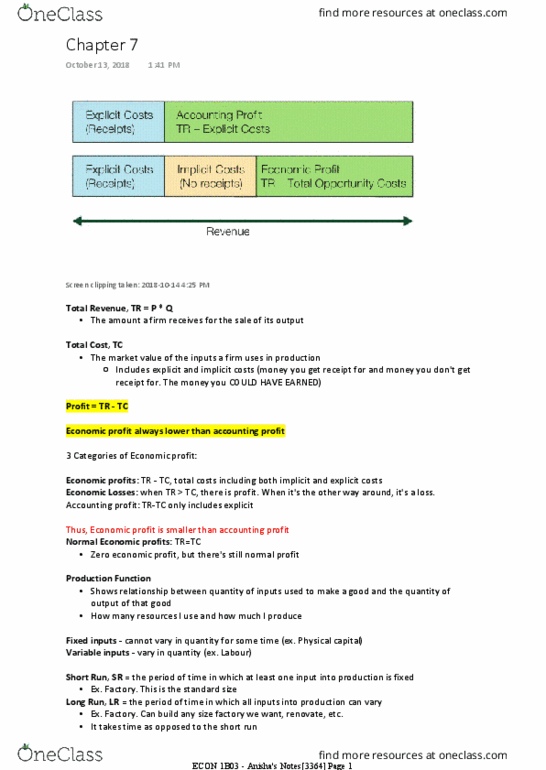

The value of all inputs the firm uses in production. You spend money and you can get a receipt for. No money involved and cannot get a receipt for it. The opportunity cost of making its output of goods and services. Total revenue - both implicit and explicit costs. Average expected profits for firms in that industry. Making zero economic profit, but a decent accounting profit. Shows the relationship between the number of inputs and the number of outputs a firm produces. Inputs that cannot vary in quantity in the short term. The period of time it takes to change the quantity of these inputs is called the short run. Ex. physical capital (the factory, or a machine) Amount output changes for an additional unit of input. Change in total output / change in # of inputs. Any additional input will decrease the total output. Too many worker get in each other way.