ECON 1B03 Lecture Notes - Lecture 8: Perfect Competition, Taipei Metro, Fixed Cost

Document Summary

Get access

Related Documents

Related Questions

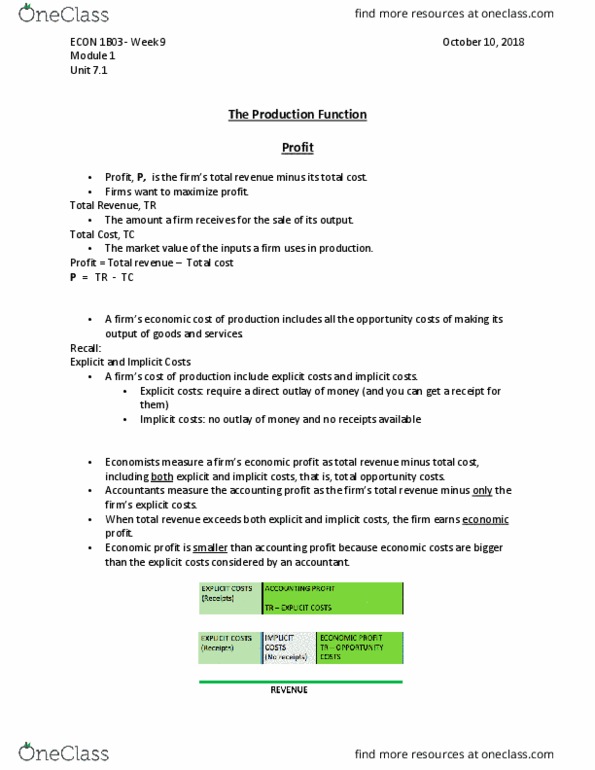

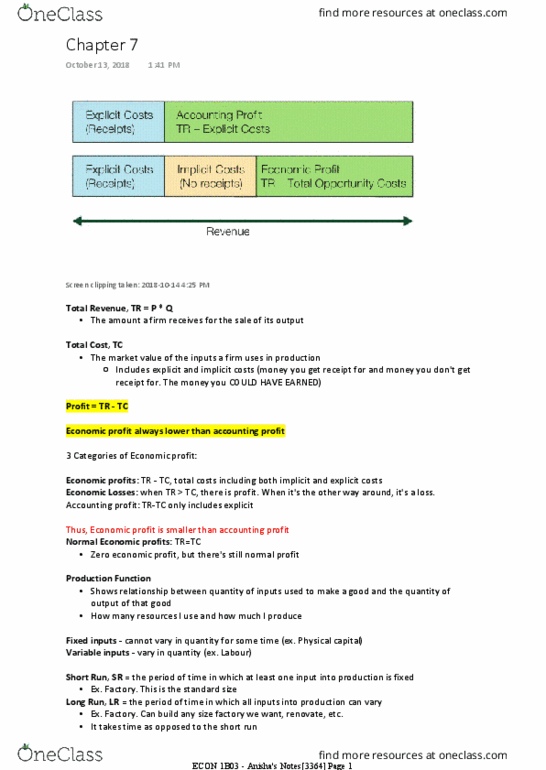

Salvatore Chapter 1:

Discussion Questions: 9. How is the concept of a normal return on investment related to the distinction between business and economic profit?

Problems:

5. Determine which of the two investment projects a manager should choose if the discount rate of the firm is 10%. The first project promises a profit of $100,000 in each of the next 4 years, while the second project promises a profit of $75,000 in each of the next 6 years.

6. Determine which of the two investment projects of Problem 5 the manager should choose if the discount rate of the firm is 20%.

15. Integration Problem Samantha Roberts has a job as a pharmacist earning $30,000 per year, and she is deciding whether to take another job as the manager of another pharmacy for $40,000 per year or to purchase a pharmacy that generates a revenue of $200,000per year. To purchase the pharmacy, Samantha would have to use her $20,000 savings and borrow another $80,000 at an interest rate of 10% per year. The pharmacy that Samantha is contemplating purchasing has additional expenses of $80,000 for supplies, $40,000 for hired help, $10,000 for rent, and $5,000 for utilities. Assume that income and business taxes are zero and that the repayment of the principle of the loan does not start before 3 years. (a) What would be the business and economic profit if Samantha purchased the pharmacy? Should Samantha purchase the pharmacy? (b) Suppose that Samantha expects that another pharmacy will open nearby at the end of 3 years and that this will drive the economic profit of the pharmacy to zero. What would the revenue of the pharmacy be in 3 years? (c) What theory of profit would account for profits being earned by the pharmacy during the first 3 years of operation? (d) Suppose that Samantha expects to sell the pharmacy at the end of 3 years for $50,000 more than the price she paid for it and that she requires a 15% return on her investment. Should she still purchase the pharmacy?

Spreadsheet Problem (see attached Excel doc)

Using the data below, (Excel doc) where column A represents student numbers, column B the finishing time for a 1 mile race for 10 students, and column C the age of the students, (a) Use the data analysis tools to plot a line graph of all the finishing times. (b) Calculate a mean, median, mode, sample variance, sample standard deviation, and coefficient of variation to statistically describe the data. (c) Use Excel to fine the covariance between the two variables. What does the covariance indicate about the relationship between finishing time and age?

Note:

P15(d): Change â⦠for $50,000 more than â¦â to â⦠for $50,000 less than â¦â Compare the present value of economic profit in each of the next three years and the loss of $50,000 in the third year using 15% as the discount rate.

The spreadsheet problem (b): Calculate a mean, â¦. to statistically describe the data of both variables, Time and Age.

Individual problems:

3-1 You won a free ticket to see a Bruce Springsteen concert (assume the ticket has no resale value). U2 has a concert the same knight, and this represents your next-best alternative activity. Tickets to the U2 concert cost $80, and on any particular day, you would be willing to pay up to $100 to see this band. Assume that there are no additional costs of seeing either show. Based on the information presented, what is the opportunity cost of seeing Bruce Springsteen?

3-3 Because of the housing bubble, many houses are now selling for much less than their selling price just 2 to 3 years ago. There is evidence that homeowners with virtually identical houses tend to ask for more is they paid more for the house. What fallacy are they making?

Salvatore Chapter 3:

Discussion Questions:

9. How would you react to a sales managerâs announcement that he or she has in place a marketing program to maximize sales?

Problems:

1(a). Given the following total-revenue function: TR= 9Q - Q^2

Derive the total-, average-, and marginal- revenue schedules from Q=0 to Q=6 by 1âs.

7. Given the total-cost schedule: Q 0 1 2 3 4

TC 1 12 14 15 20

Derive the average- and marginal-cost schedules.

9. With the total-revenue curve of Problem 1 and the total-cost curve of problem 7, derive the total-profit function and show how the firm determines the profit-maximizing level of output.

Note:

DQ9: Does maximum sales (revenue) equal maximum profit (see figure 3-4)?

Revised P1(a): Derive the total-revenue, average-revenue, and marginal-revenue schedules from Q = 0 to Q = 4 by 1s.

Average revenue (AR) = total revenue (TR)/Q

Marginal revenue (MR) = change in total revenue/change in Q

For example:

| Q | TR | AR | MR |

| 2 | 14 | 7 (=14/2) | |

| 3 | 18 | 6 (=18/3) | 4 (=(18-14)/(3-2) |

Revised P9: With the total-revenue schedule of Problem 1 and the total-cost schedule of Problem 7, show the profit-maximizing level of output (profit=TR-TC).

Froeb et al. Chapter 4:

Individual problems:

4-5 Your insurance firm processes claims through its newer, larger high-tech facility and its older, smaller low-tech facility. Each month, the high-tech facility handles 10,000 claims, incurs $100,000 in fixed costs and $100,000 in variable costs. Each month, the low-tech facility handles 2,000 claims, incurs $16,000 in fixed costs and $24,000 in variable costs. If you anticipate a decrease in the number of claims, where will you lay off workers?

4-6 A copier company wants to expand production. It currently has 20 workers who share eight copiers. Two months ago, the firm added two new copiers, and output increased by 100,000 pages per day. One month ago, they added five workers, and productivity also increased by 50,000 pages per day. Copiers cost about twice as much as workers. Would you recommend they hire another employee or buy another copier?