ACC 100 Lecture Notes - Lecture 1: Cost Leadership, Total Quality Management, Management Accounting

8 Aug 2016

School

Department

Course

Professor

Document Summary

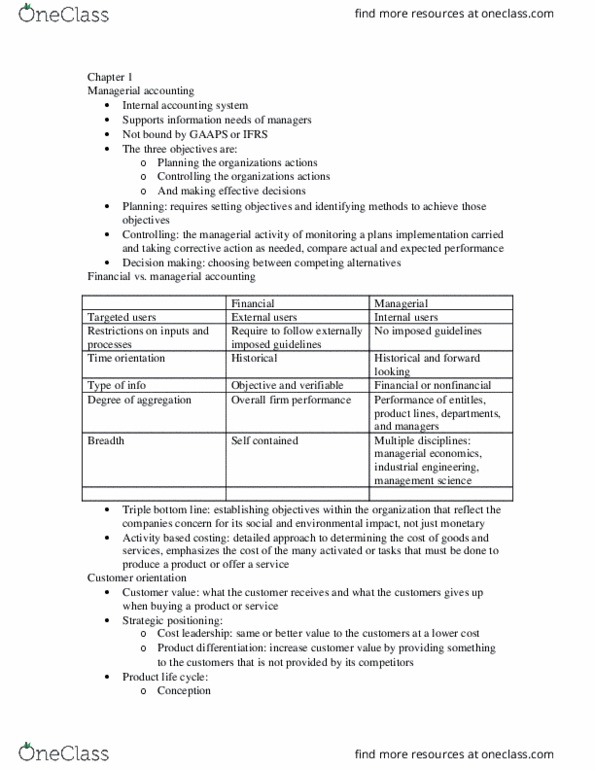

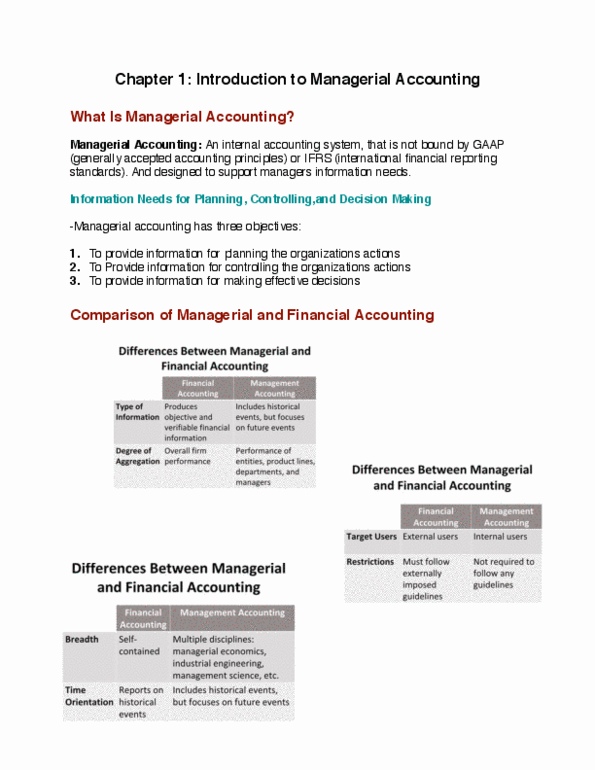

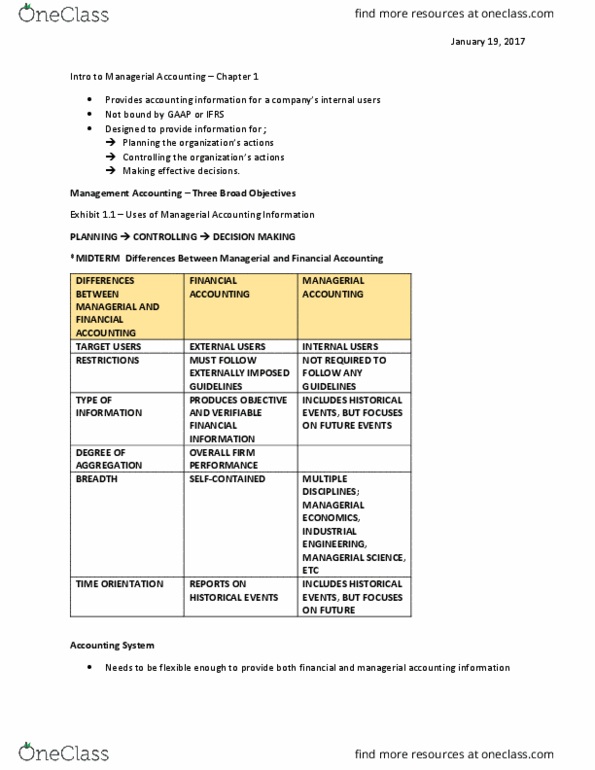

Managerial accounting: an internal accounting system not bound by gaap or ifrs designed to support managers" information needs. Performance of entities product lines, departments and managers. Multiple disciplines; managerial economics, industrial engineering, management science, etc. Includes historical events but focuses on future events. Accounting system: flexible enough to provide financial and managerial accounting information to supply information for different purposes. Current focus: developments in technology, transportation and communication have created the need for better information. In response, the need for better information, activity based management accounting system were developed. Indirect cost allocation first stage allocation second stage allocation cost objective. More detailed approach to determining cost of goods and services. Emphasizes cost of many activities or tasks that must be done to product a product. Objective: find ways to perform necessary activities more efficiently and eliminate those that do not create customer value. Advantages come when the company can create better customer value.