ACC 110 Lecture Notes - Fiscal Year, Intangible Asset, Retained Earnings

6 Oct 2012

School

Department

Course

Professor

Document Summary

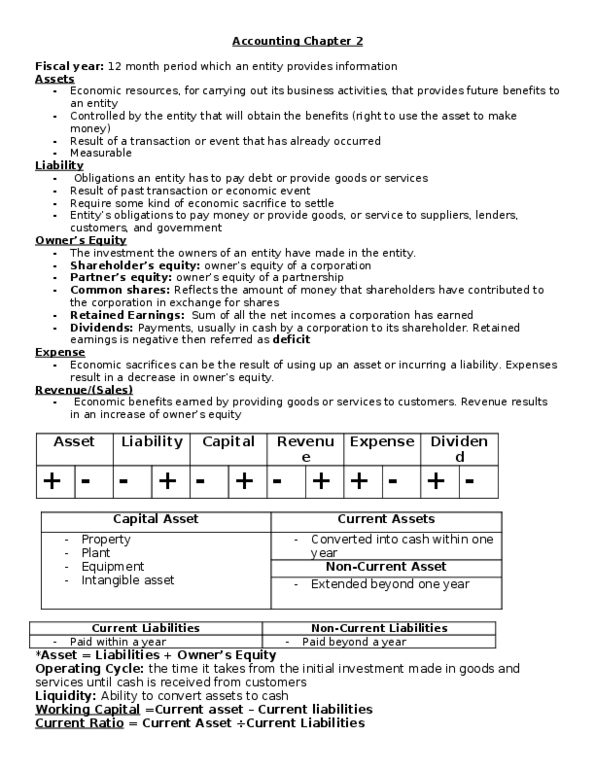

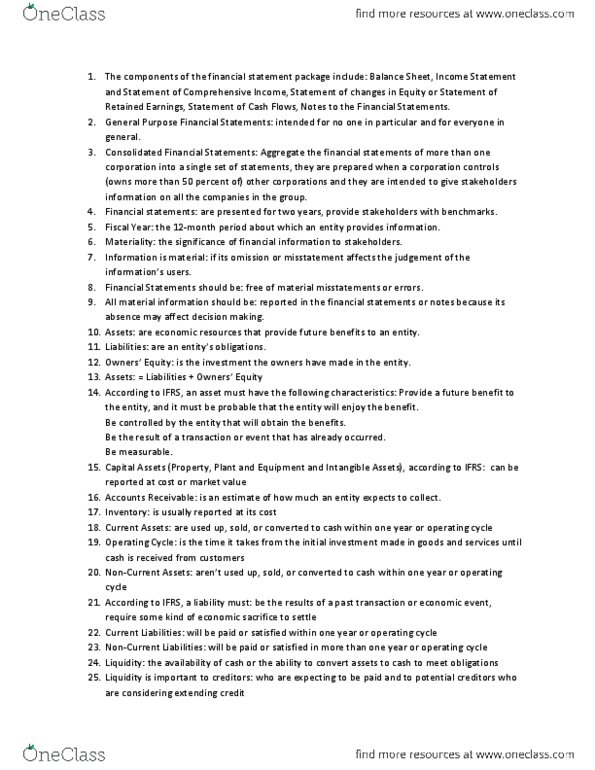

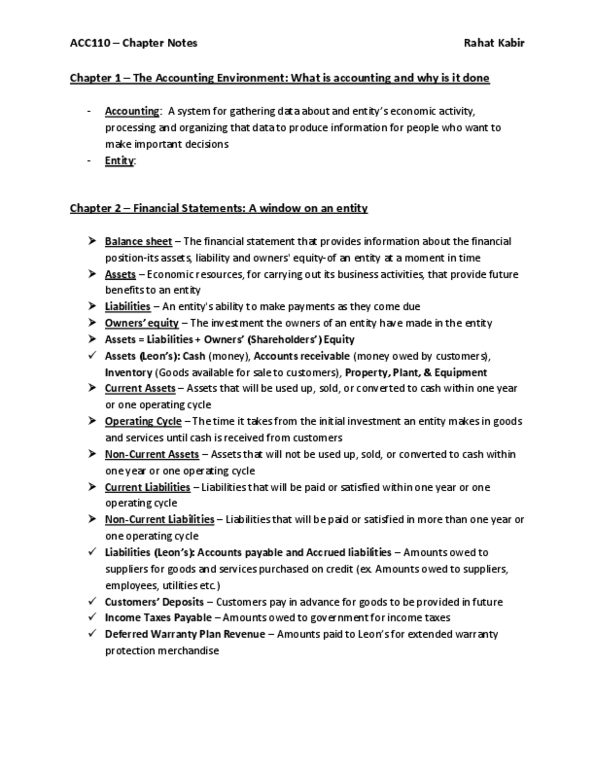

Fiscal year: 12 month period which an entity provides information. Economic resources, for carrying out its business activities, that provides future benefits to an entity. Controlled by the entity that will obtain the benefits (right to use the asset to make money) Result of a transaction or event that has already occurred. Obligations an entity has to pay debt or provide goods or services. Result of past transaction or economic event. Require some kind of economic sacrifice to settle. Entity"s obligations to pay money or provide goods, or service to suppliers, lenders, customers, and government. The investment the owners of an entity have made in the entity. Shareholder"s equity: owner"s equity of a corporation. Partner"s equity: owner"s equity of a partnership. Common shares: reflects the amount of money that shareholders have contributed to the corporation in exchange for shares. Retained earnings: sum of all the net incomes a corporation has earned.