ACC 406 Lecture Notes - Lecture 2: Komala Party Of Iranian Kurdistan, Gross Margin, Management Accounting

23 Feb 2017

School

Department

Course

Professor

Document Summary

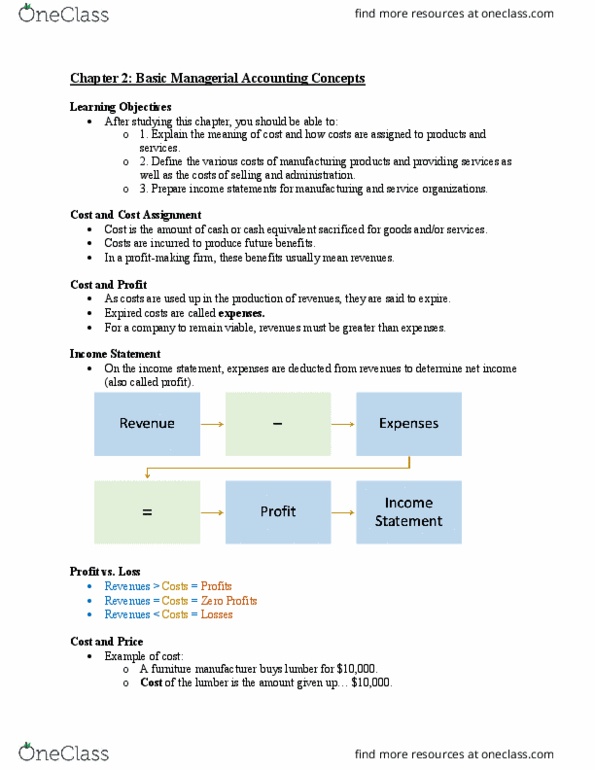

Intro to managerial accounting; cost behaviour (chapter 2&3) Cost is the amount of cash or cash equivalent sacrificed for goods and/or services. Costs are incurred to produce future benefits. Costs must be split and arranged: time is an opportunity cost. Textbooks: costs are just like music, break them into different groups, call them different things because you use to them to make different decisions, same song may be in two different playlists, just like costs. In a profit-making firm, these benefits usually mean revenues. As costs are used up in the production of revenues, they are said to expire. For a company to remain viable, revenues must be greater than expenses. On the income statement, expenses are deducted from revenues to determine income (also called profit). Revenues expenses = profit income statement. Cost of the lumber is the amount given up ,000. Price is the amount we charge our customers for our products or services.