ACC 406 Lecture Notes - Lecture 7: Management Accounting, Finished Good

14 Mar 2017

School

Department

Course

Professor

Document Summary

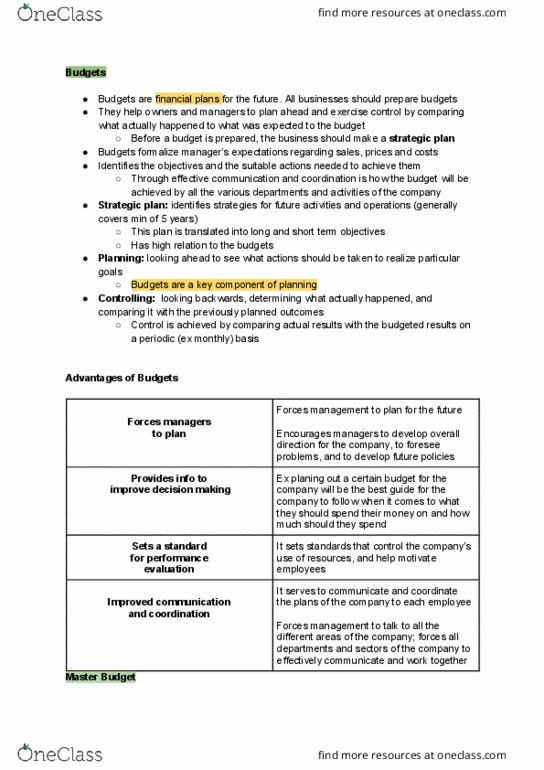

Strategic plan: before a budget is prepared, a strategic plan should be developed, identi es strategies for future activities and operations, need to have long and short term objectives, objectives for the basis of the budget. Sales budget preparation steps: develop a sales forecast - responsibility of marketing department; use bottom-up approach and salespeople submit sales projections, forecast is reviewed by a budget committee, budget committee recommends changes prior to approval. Budget committee: reviews the budgets, provides policy guidelines and budgetary goals, resolves differences that arise as the budget is prepared, approves the nal budget, monitors actual performance as the year unfolds. Production budget: describes how manhunts must be reduced in order to meet sales needs and satisfy ending inventory requirements, units to be produced = expected unit sales + units in ending inventory - units in beginning inventory. Direct materials purchases budget: tells the amount and cost of raw material to be purchased in each time period.