ACC 110 Lecture Notes - Income Statement, Kynoch, Write-Off

6 Oct 2012

School

Department

Course

Professor

Document Summary

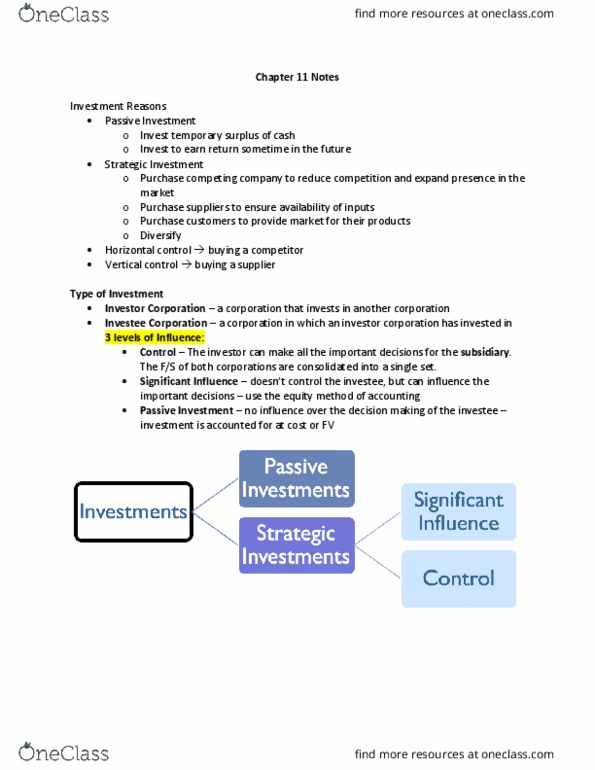

E11-1. a: the investor has control (owning more than 50%) over the investee corporation. Therefore, consolidated financial statements should be prepared. c. If the 25% ownership of shares represents 25% of the votes, this investment would be classified as an equity investment if the investor has significant influence on the decision making of the investee. Ifrs suggests that owning between 20% and 50% of the votes of an investee company is an indication of significant influence. The investment could be classified as available-for-sale or trading, depending on the intent of management. (equity investments cannot be classified as held-to-maturity. ) Available-for-sale and trading investments are reported on the balance sheet at their fair value. The non-controlling interest would be 25% of the fair value of the net assets or 25% of ,600,000 which is ,000. b. The assets and liabilities would appear at 100% of their fair value. To record the purchase of 2,000 shares of inwood corp. (2,000 shares )