ACC 110 Lecture Notes - Financial Statement, Income Statement, Deferred Tax

6 Oct 2012

School

Department

Course

Professor

Document Summary

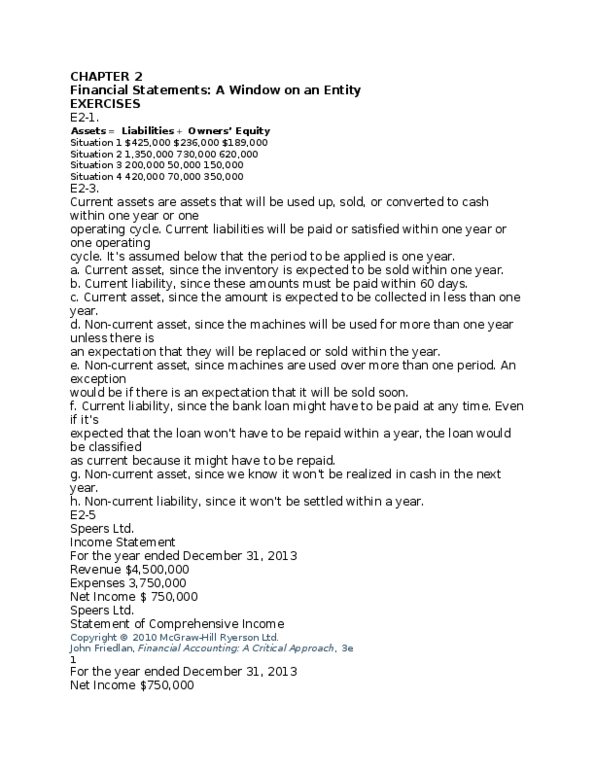

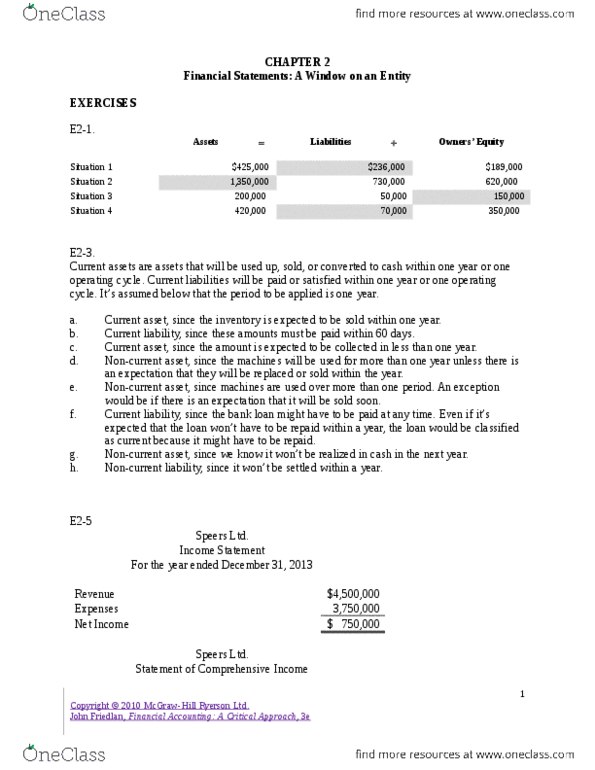

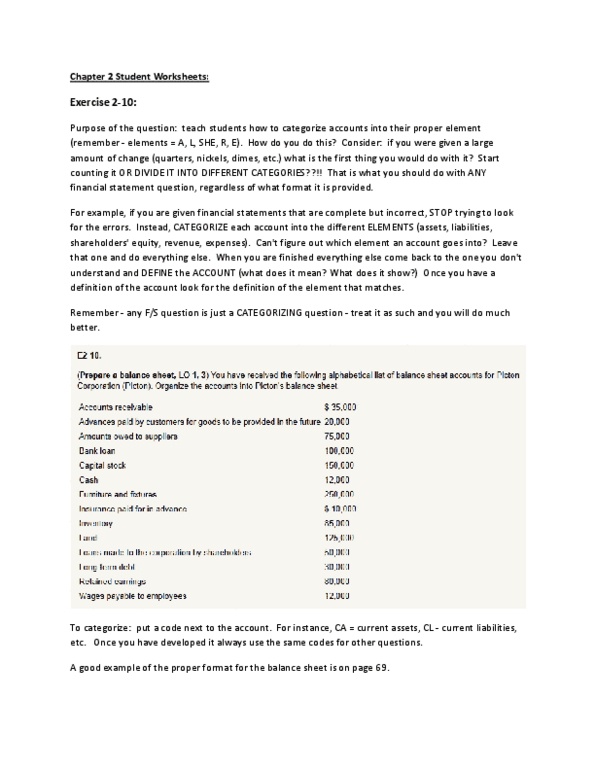

Current assets are assets that will be used up, sold, or converted to cash within one year or one operating cycle. Current liabilities will be paid or satisfied within one year or one operating cycle. It"s assumed below that the period to be applied is one year. a. b. c. d. e. f. g. h. Current asset, since the inventory is expected to be sold within one year. Current liability, since these amounts must be paid within 60 days. Current asset, since the amount is expected to be collected in less than one year. Non-current asset, since the machines will be used for more than one year unless there is an expectation that they will be replaced or sold within the year. Non-current asset, since machines are used over more than one period. An exception would be if there is an expectation that it will be sold soon.