FIN 300 Lecture Notes - Lecture 2: Operating Cash Flow, Capital Cost Allowance, Cash Flow

24 Jan 2017

School

Department

Course

Professor

Chapter Cot’d

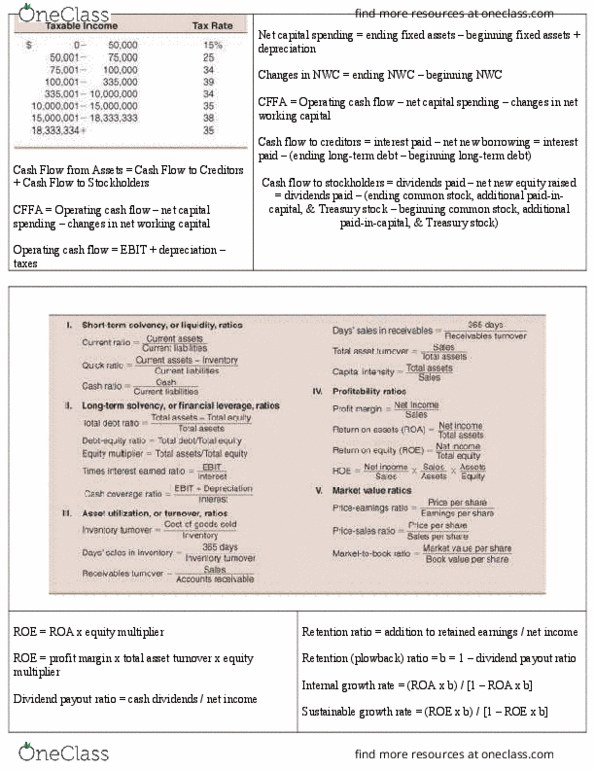

Cash Flow Identity (Cash flow from assets) CFFA = Cash flow to creditors + Cashflow to shareholders

Cash flow from assets (Cash flow from assets) = Operating cash flow – net capital spending – additions

to net working capital (NWC)

Operating cash flow OCF= Earnings before interest and taxed + depreciation – taxes

Net capital spending = ending net fixed assets – beginning next fixed assets + depreciation

Additions to NWC = Ending NWC – Beginning NWC

Working Capital = Current Assets – Current Liabilities

Using Table from 2.1

Ex. Creditors = Int.Paid(Income statement) – Net New Borrowing(Long term debt) (Balance sheet) = $70-

(454-408)= $24

S/H = Dividends(Income Statement) – Net New Equity(common shares)(Balance sheet) = $65 –(640-

600)= $25

CFFA = 24+25 = $49

Ex. Operating Cash Flow = EBIT(I/S) + depreciation(I/S) – taxes(I/S) = 694 + 65 – 250 = $509

Ex.Net Capital Spending = End NFA – Beg NFA + Depreciation = 1709 – 1644 + 65 = $130

Ex Additions to NWC = End NWC – Beg NWC = (1403 – 389) – (1112 – 428)=1014 – 684 = $330

Ex Cash flow from assets = OCF – NCS – NWC = 509 – 130 – 330 = $49

Capital Cost Allowance

- CCA is depreciation for tax purposes

- CCA is deducted before taxes and acts as a tax shield

- Every asset is given a certain class, what rate to depreciate and how to depreciate.

- Half year Rule – first year only half of assets cost can be used for CCA

Chapter 3

Sources and Uses of Cash

- Sources

o Cash inflow occurs when we sell something

o Decrease in assets account increase in liability or equity

- Uses

o Cash outflow – ours whe we uy soethig

o Increase in asset account

o Decrease in liability or equity

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Cash flow identity (cash flow from assets) cffa = cash flow to creditors + cashflow to shareholders. Cash flow from assets (cash flow from assets) = operating cash flow net capital spending additions to net working capital (nwc) Operating cash flow ocf= earnings before interest and taxed + depreciation taxes. Net capital spending = ending net fixed assets beginning next fixed assets + depreciation. Additions to nwc = ending nwc beginning nwc. Working capital = current assets current liabilities. Creditors = int. paid(income statement) net new borrowing(long term debt) (balance sheet) = - (454-408)= . S/h = dividends(income statement) net new equity(common shares)(balance sheet) = (640- Operating cash flow = ebit(i/s) + depreciation(i/s) taxes(i/s) = 694 + 65 250 = . Ex. net capital spending = end nfa beg nfa + depreciation = 1709 1644 + 65 = . Ex additions to nwc = end nwc beg nwc = (1403 389) (1112 428)=1014 684 = .