FIN 501 Lecture Notes - Lecture 15: Cope

20 Nov 2014

School

Department

Course

Professor

Document Summary

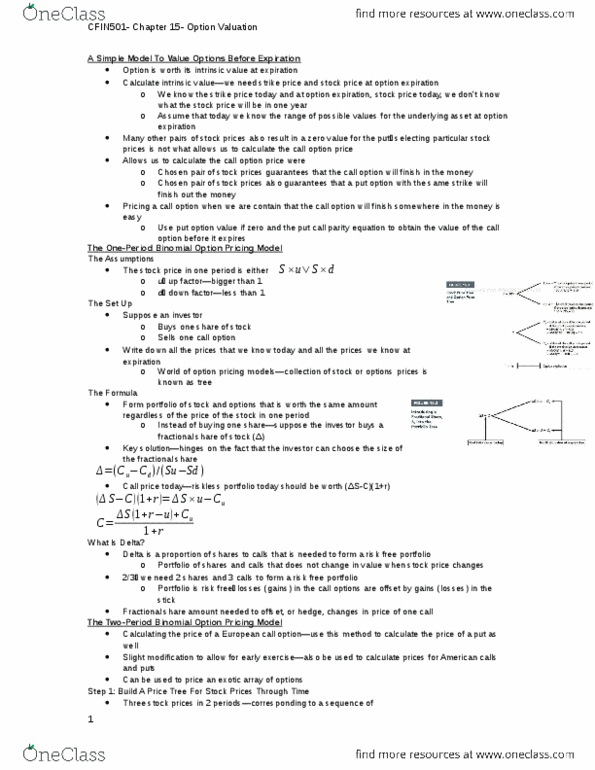

If you know the price of similar put, you can use put-call parity to price call option before it expires. 15. 2 1 period binomial option pricing model (bopm) o o o. The fractional share amount needed to hedge 1 call. # of calls to hedge 1 share = C value of call in 1 period u up factor d r down factor risk free rate. Allows to calculate price of call option before maturity (and, no put price is needed) Calculates price of european options on non-dividend paying stocks. S current price of the underlying stock. K strike price specified in option k. R risk-free interest rate over life of option. T time remaining until option expires s price volatility of underlying stock. ; only 1 that is not directly observable. Price of call option on 1 share of cs o. Price of put option on 1 share of cs. Verify : c p = s ke rt.