LAW 603 Lecture Notes - Lecture 3: Canada Revenue Agency, Fiduciary, Environment And Climate Change Canada

28 May 2018

School

Department

Course

Professor

Lecture 3 - Basic Forms of Business Organizations

Tuesday, January 30, 2018

3:08 PM

Basic Forms of Business Organization

• Sole Proprietorship

• Partnership

o General Partnership

o Limited Partnership

o Limited Liability Partnership

• Corporation

Sole Proprietorship

• A sole proprietor conducts business in his or her own name. There is no separate legal structure or

separation between the owner and the business on any level.

o The owner is exclusively and personally responsible for conducting the business;

o The owner is exclusively and personally liable for all torts and contractual or other breaches

in regard to the business;

o Money earned goes to you;

o Everything you own is at risk, all debts incurred against the business is also considered

personal debt

• Advantages

o It is the simplest and least costly form of business to establish and operate;

o It is the simplest and least costly to dissolve.

• Disadvantages

o The owner risks unrestricted and unlimited personal liability.

Partnership

• Legal Characteristics

o Two or more people carry on a business to make a profit;

o By definition, partnership is not an available form of business for non-profit organizations.

Corporation

• A corporation is the most common form of business organization.

• Federal or provincial incorporation:

o Canada Business Corporations Act (CBCA) or

o Ontario Business Corporations Act (OBCA)

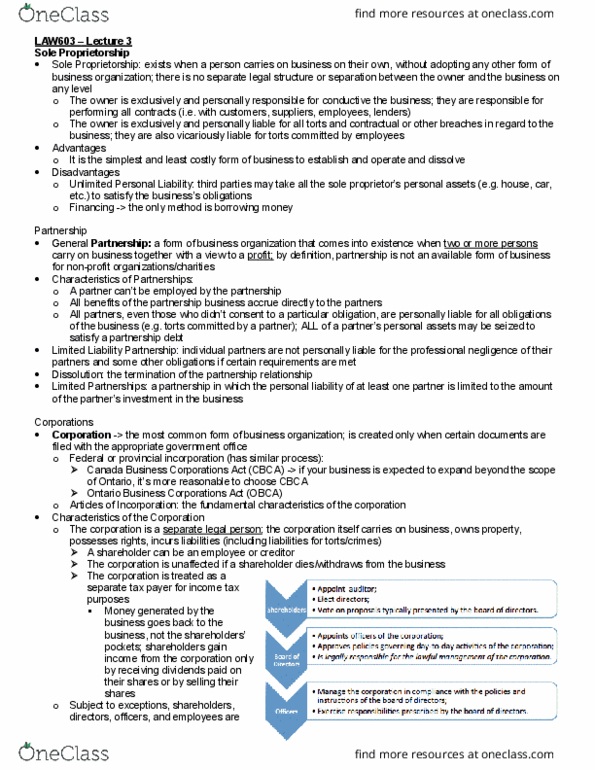

• Characteristics of the Corporation

o The corporation is a separate legal person

o The corporation (not shareholders, officers or directors) carries on business, incurs

liabilities, and generates revenue, profits, losses, etc.;

o The corporation has separate income and tax status. Shareholders gain income from the

corporation only by receiving dividends paid on their shares or by selling their shares;

o Subject to exceptions, shareholders, directors, officers and employees (slide 13)

o The corporation has separate income and tax status. Shareholders gain income from the

corporation only by receiving dividends paid on their shares or by selling their shares;

find more resources at oneclass.com

find more resources at oneclass.com

o Subject to exceptions, shareholders, directors, officers and employees are not personally

liable for the actions of the corporation;

o Ownership is separate from management.

▪ Shareholders elect directors who, in turn, appoint officers to manage the business;

▪ Subject to a Unanimous Shareholders Agreement, the legal responsibility for managing

resides with the board of directors (not the officers and not the shareholders).

• Fiduciary duty

• This concept exists at common law as well as in statute.

o Eah diretor and officer in exercising his powers and discharging his duties shall . . . act

honestly and in good faith with a view to the best interests of the corporation. . . .

[CBCA, s. 122 (1) (a)]

• The OBCA has a comparable provision. [s. 134]

• Duty of Care

o CBCA s. 122 (1)(b); OBCA s. 134 (1)(b);

o Directors and officers are required to exercise the care, diligence and skill that a reasonably

prudent person would exercise in comparable circumstances.

Non-Profit and Charity Organizations

• Similarities

o Both operate on a non-profit basis;

o Neither can distribute its income to members, directors, officers or trustees;

o Both are exempt from taxation on their income.

What is a Charity?

• A charity must be engaged in the following:

o Relief of poverty;

o Advancement of education;

o Advancement of religion;

o Other purposes beneficial to the community.

• Source

o Special Commissioners of Income Tax v. Pemsel, [1891] A.C. 531 (H.L.)

o Vancouver Society of Immigrant and Visible Minority Women v. Canada (Minister of National

Revenue-M.N.R.), [1999] 1 S.C.R. 10

• A charity can take only one of the following forms:

find more resources at oneclass.com

find more resources at oneclass.com

o Charitable organization;

o Public foundation;

o Private foundation;

• Only a registered charity can issue receipts to donors for income tax purposes.

• Have to register as a charity through the CRA (Canadian Revenue Agency)

• Non-profits cannot issue receipts for tax purposes

What is a Non-Profit?

• A non-profit can pursue a broader mandate than a charity.

o Under the Income Tax Act, R.S.C. 1985, c. 1 (5th Supp), a non-profit organization is defined as

. . . ot a harit . . . orgaized ad operated elusiel for soial elfare, ii

iproeet, pleasure or rereatio or for a other purpose eept profit. . . . (p. 153)

o E.g., recreational, social and arts organizations

o Any profits made has to be re-distributed to their stated purpose

o Your organization cannot be both a charity and non-profit according to the Income Tax Act.

Federal Legal Environment

• Canada Not-for-profit Corporations Act, S.C, 2009, c. 23

o This statute covers the incorporation and general governance of federal non-share capital

corporations;

o It includes the requirements for incorporation, its capacity and powers, eligibility, roles and

responsibilities of officers and directors, etc.

• Income Tax Act, R.S.C. 1985, c. 1 (5th Supp)

o Determines whether an organization is a charity or a non-profit organization;

o Places certain obligations on directors of organizations.

• Charities Registration (Security Information) Act, S.C. 2001, c. 41

o Post-9/11 legislation to ensure charities do not fund terrorist activities.

• Competition Act, R.S.C. 1985, c-34

o Provides rules for regulating the fundraising activities of charities.

• Lobbying Act, R.S.C. 1985, c. 44 (4th Supp.)

o Charities are included with organizations that must register with the government and file an

annual return if they communicate with public office-holders in regard to changes to the law

or other public policy matters.

Ontario Legal Environment

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Lecture 3 - basic forms of business organizations. Sole proprietorship: partnership, general partnership, limited partnership, limited liability partnership, corporation. Sole proprietorship: a sole proprietor conducts business in his or her own name. It is the simplest and least costly form of business to establish and operate; It is the simplest and least costly to dissolve: disadvantages, the owner risks unrestricted and unlimited personal liability. Legal characteristics: two or more people carry on a business to make a profit, by definition, partnership is not an available form of business for non-profit organizations. Corporation: a corporation is the most common form of business organization. Shareholders gain income from the corporation only by receiving dividends paid on their shares or by selling their shares: subject to exceptions, shareholders, directors, officers and employees (slide 13, the corporation has separate income and tax status. Shareholders elect directors who, in turn, appoint officers to manage the business;