NPM700 Lecture Notes - Lecture 2: Share Capital, Fiduciary, Tax Avoidance

Document Summary

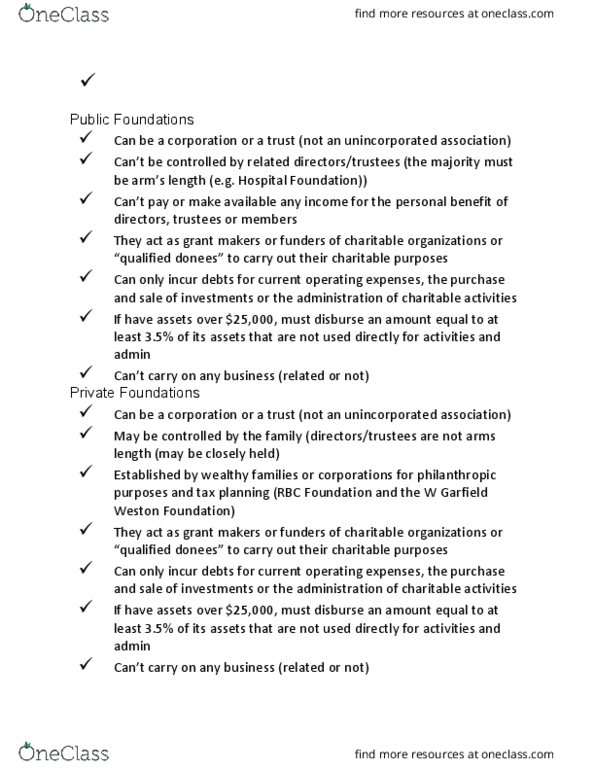

Can be corporation, unincorporated association, or a trust. Can"t be controlled by a group of related directors/trustees. Can"t pay or make available any income for the personal benefit of directors or members. Permitted to control a corporation (may operate a business through a taxable share capital corporation) as long as it"s a related business (linked and subordinate to the charity). If have assets over ,000, must disburse an amount equal to at least 3. 5% of its assets that are not used directly for activities and admin. Can"t be controlled by related directors/trustees (the majority must be arm"s length (e. g. hospital foundation)) Can"t pay or make available any income for the personal benefit of directors, trustees or members. Can be a corporation or a trust (not an unincorporated association) May be controlled by the family (directors/trustees are not arms length (may be closely held)