BUS 251 Lecture Notes - Lecture 3: Income Statement, Cash Cash, Accounts Receivable

21 Feb 2017

School

Department

Course

Professor

Document Summary

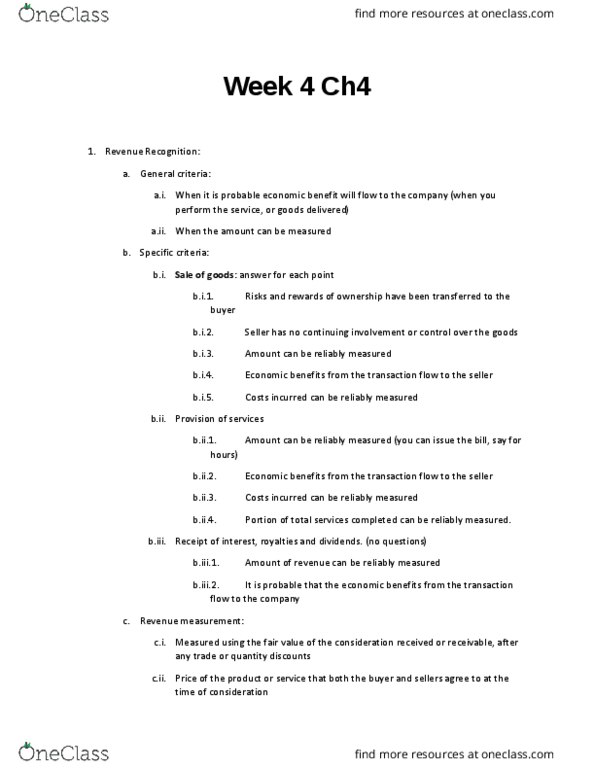

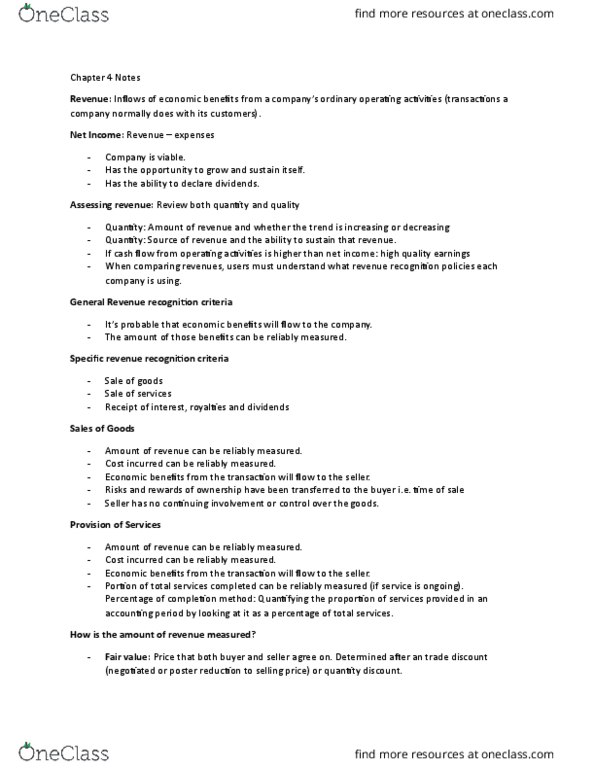

Management has a big hand on deciding revenue recognition. General revenue recognition criteria (you will benefit and know how much you benefit) It is probably that economic benefits will flow to company. The amount of benefits can be measured reliably (when do you know you will benefit) Specific revenue recognition criteria for 3 common strategies of revenue generating activities: sales of goods; provision of services; receipt of interest, royalties and dividends. Risk and rewards of ownership transfers to buyer. Providing services iii, iv, v +duration of service completed can be measured. Interest, royalties and dividends: iii, iv (the basic two revenue recognition guidelines) Measured using the fair value of consideration received or receivable, after any trade or quantity discounts (recorded in journal entries) Fair value = price of product or service that both buyers and sellers agree to. Sales discounts (credit sales (100k), debit accounts receivable (90k), debit sales discount expense (10k))