BUS 251 Lecture Notes - Lecture 5: Cash Flow Statement, Accrual, Cash Flow

14 May 2016

School

Department

Course

Professor

Document Summary

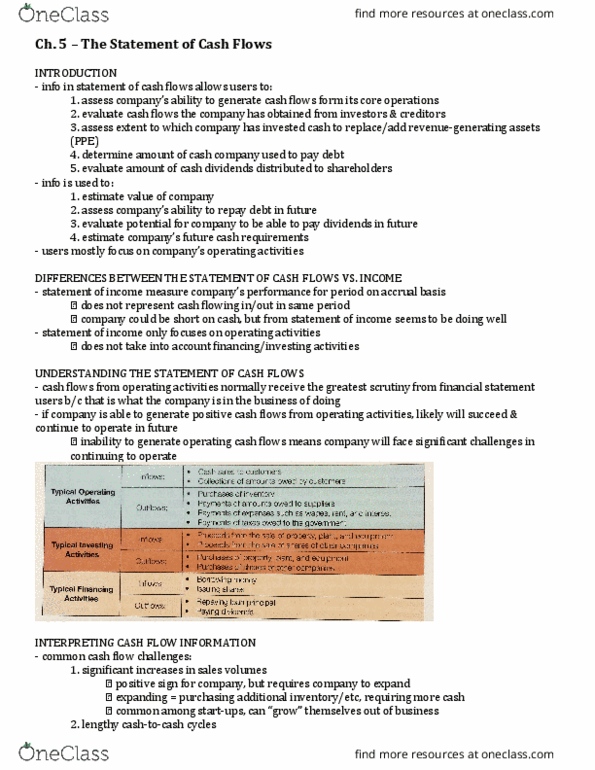

Understand and analyze cash-flows but don"t have to make them. Exibit 5-1: significance of cash flow statement helps us, retrospectively a. i. Assess the company"s ability to generate cash flows from operations a. ii. Evaluate where cash has come from debt or equity a. iii. Assess level and type of capital assets investments a. iv. Determine how much cash was used for debt repayment a. v. Evaluate the distribution of cash dividends: prospectively b. i. Estimate the value of the company based on cash flows b. ii. Assess the company"s ability to repay debt in the future b. iii. Evaluate the potential for dividend payments in the future b. iv. All other transactions not covered by financing or invsting activities a. ii. They are result of day to day business operations a. ii. 2. They are the source for furutre debt repayment a. ii. 3. They are the source for future dividend payments b. Investment, sale, or disposal of long-term assets b. ii. Examples: property, plant, equipment, long-term marketable securities c.