BUS 254 Lecture Notes - Lecture 8: Net Income, Total Absorption Costing, Financial Statement

18 Sep 2018

School

Department

Course

Professor

3

BUS 254 Full Course Notes

Verified Note

3 documents

Document Summary

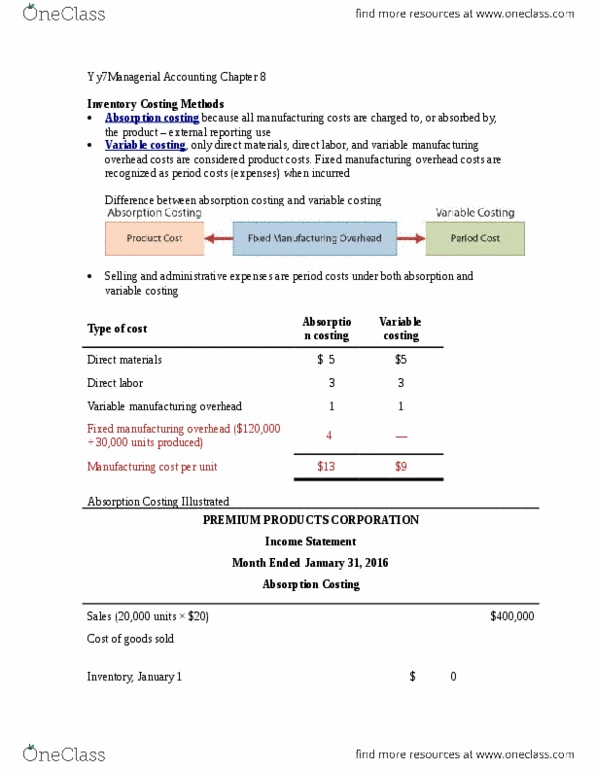

Cost of goods sold ([ + ] x 1700 units) Fixed overhead ,000 / 1700 units = per unit. Variable selling and administrative expenses (,500 x 6%) Variable cost of goods sold (1700 units x ) 23,650: the difference in net income of ,500 can be explained by the 300 u(cid:374)its" difference between the number of units sold (1,700) and the number of units produced (2,000). Under absorption costing, the company defers per unit of fixed manufacturing costs in the 300 units of ending inventory. This represents the total difference of ,500 (300 x ) between the net income under variable costing (,650) and under absorption costing (,150). Advantages of variable costing: the use of variable costing is consistent with the cvp material and incremental analysis, net income calculated under variable costing is not affected by changes in production levels.