BUS 312 Lecture Notes - Lecture 9: Squared Deviations From The Mean, Risk Premium, Idiosyncrasy

4 Dec 2018

School

Department

Course

Professor

Document Summary

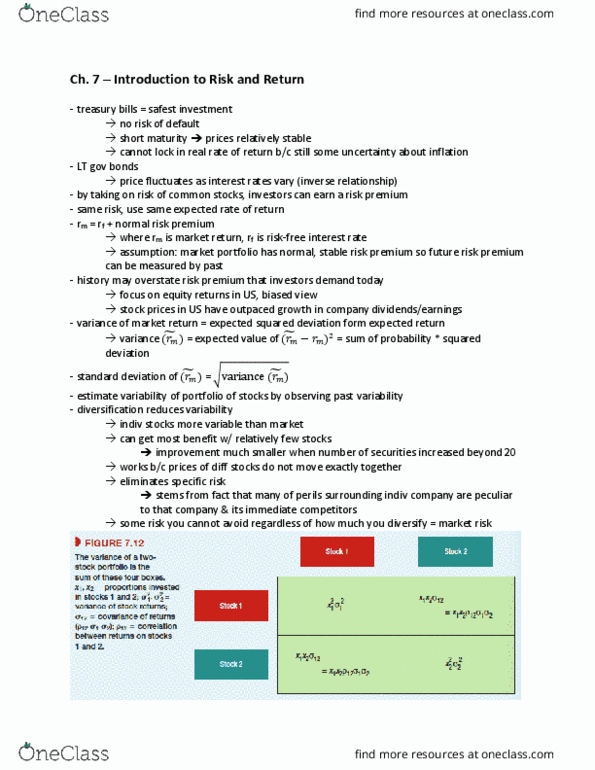

Risk premium=e(r)-rf return of individual securities r= p1 + d1 - p0 p0. Nominal return on stocks minus nominal returns on bills. Measuring risk histogram of annual u. s. stock market returns (1900-2011) A note on calculating variance and covariance: when variance (or covariance) is estimated from a sample of observed returns, the squared deviations are usually divided by n-1, where n is the number of observations. Market risk by country (1900-2011) standard deviation of annual returns, % standard deviation of annual returns. The effect of diversification average risk of portfolios containing different numbers of stocks. Stocks in each portfolio were selected randomly from the us stock market between 2006 and. Measuring risk diversification strategy designed to reduce risk by spreading the portfolio across many investments. Specific risk risk factors affecting only that firm. Idiosyncratic risk or diversifiable risk. market risk economy-wide sources of risk that affect the overall stock market. Then we have: extend easily to portfolio of n assets.