BUS 320 Lecture Notes - Lecture 11: Impaired Asset, Book Value, Cash Flow

17 Jan 2018

School

Department

Course

Professor

Document Summary

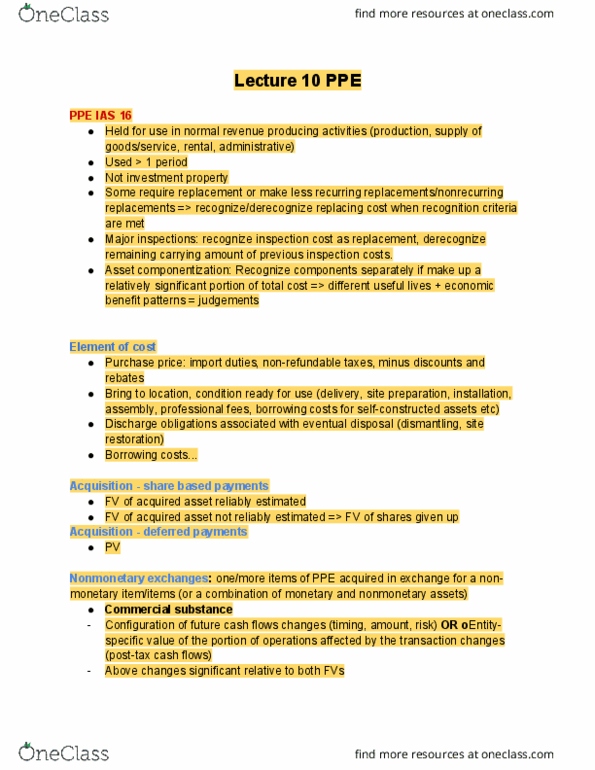

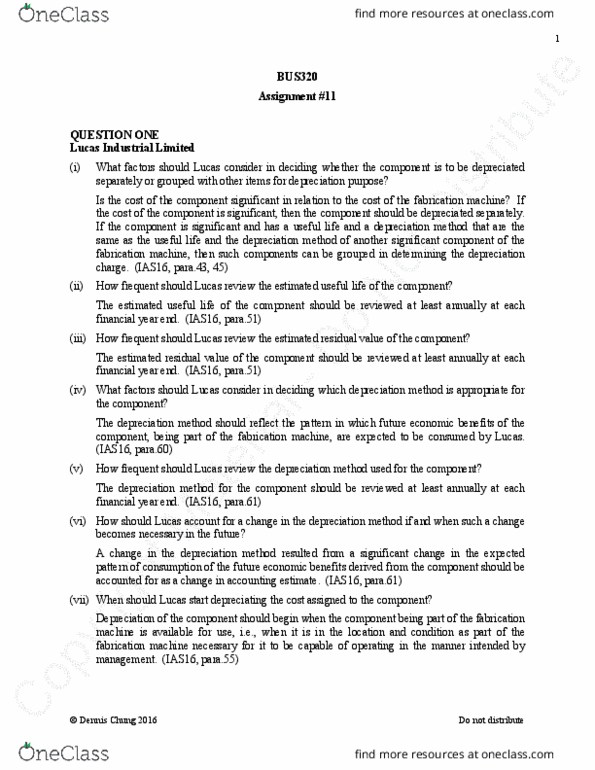

Depreciation ias 16: systematic allocation of depreciable amount over useful life. Carrying amount = cost - accumulated depreciations - accumulated impairment losses. Separate depreciation: asset componentization(group if same useful lives and depreciation methods) Recognized in profit/loss unless included in carrying amount of other assets (cost of inventories in manufacturing process => cogs in is when product sold) 0 depreciation if residual value >= carrying amount until <= carrying amount. Useful life, residual value, depreciation method reflecting pattern of consumption of future economic benefits review at least annually at fiscal year end => change = adjust prospectively as change in accounting estimate ias 8. => start: available for use (in location/condition necessary for it to be capable of operating in a manner intended by management) (not idle/retire unless fully depreciated) (can be 0 if no production for usage method) =>ceases: at the earlier of the date-held for sale (meet requirements ifrs 5 for discontinued operations) or derecognized (dispose/sold)