BUS 320 Lecture Notes - Lecture 2: Retained Earnings, Financial Statement, Comprehensive Income

3 Sep 2015

School

Department

Course

Professor

Document Summary

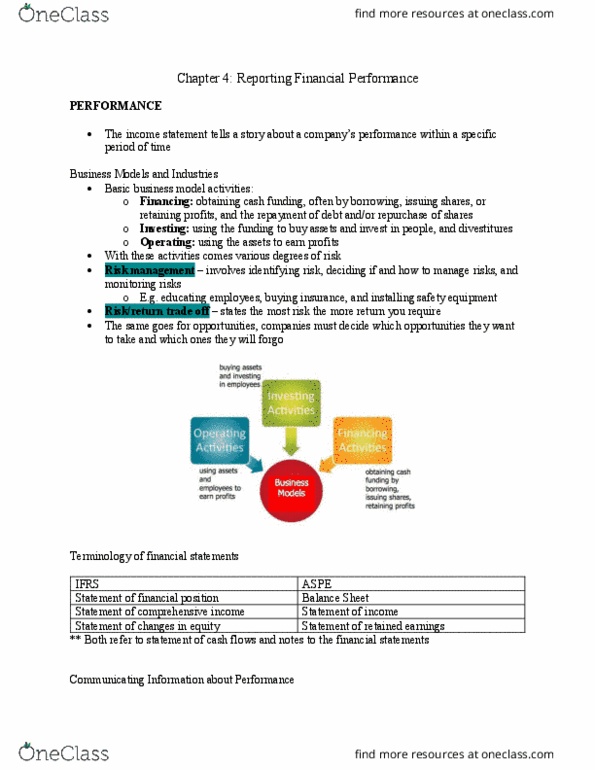

Obtain cash funding from borrowing, issuing shares, or retaining profits. Involve the repayment of debt and repurchase of shares. Use the funding to buy assets and invest in people. Help assess the risk or uncertainty of future net cash flows. Results from continuing operations are useful because operations are the primary source to generate cash and revenues. Soft numbers: difficult to measure (provision of bad debts) Hard numbers: easily measured with some level of certainty. Items that cannot be measured reliably are not reported. Many items are not properly represented in the financial statements. Refer to how solid the earnings numbers are. Used to assess how well the income reflects the underlying business and future potential. If the quality is low (high), the numbers are discounted (accepted) The earnings generated from ongoing core business activities. Based on sound business strategy and business model. Identify the effects on earnings stability, volatility, and sustainability.