BUS 322 Lecture Notes - Lecture 5: Financial Statement

13 Nov 2016

School

Department

Course

Professor

Document Summary

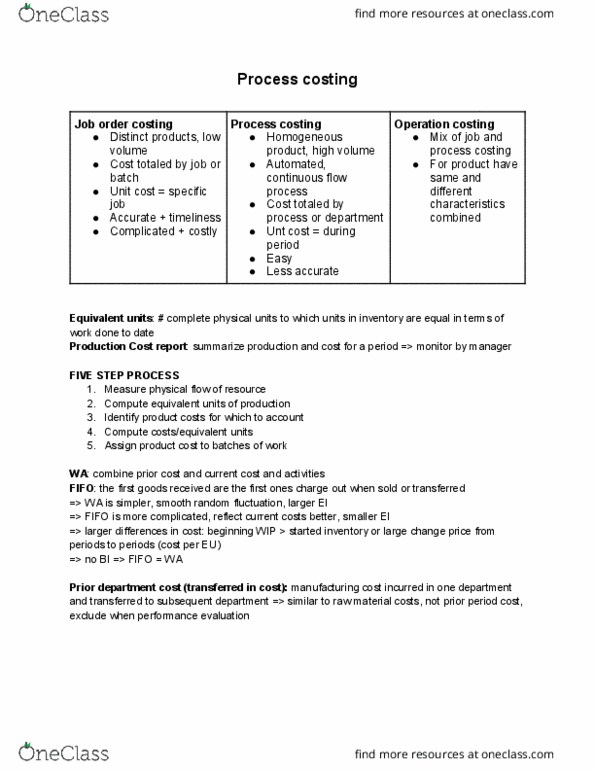

A method for assigning product costs to units of product when all units of product are virtually the same. Products are completed in a short time, and costs for a single period can be averaged over the number of units produced. Costs are not traced to units of product, instead all production costs are assigned allocated based on total production costs and total units produced. If they are costly, they need to be redesigned or dropped. To determine the value of inventory for financial reporting. Objective (same) determine the cost of products. Inventory accounts (same) raw materials, work in process, and finished goods. Overhead assignment method (same) predetermined rate actual activity. Many unique high costs jobs are built to. A few identical , low cost products continuously customer order. Work in process has a job cost record for produced for inventory in automated process. Work in process has a production report for each individual jobs batch of products.