BUS 320 Lecture Notes - Lecture 4: Revenue Recognition, Credit Risk

17 Jan 2018

School

Department

Course

Professor

Document Summary

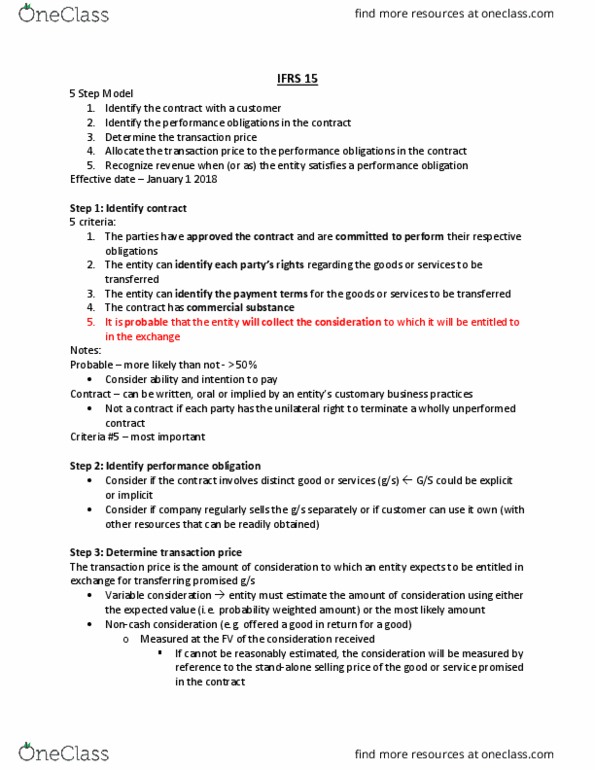

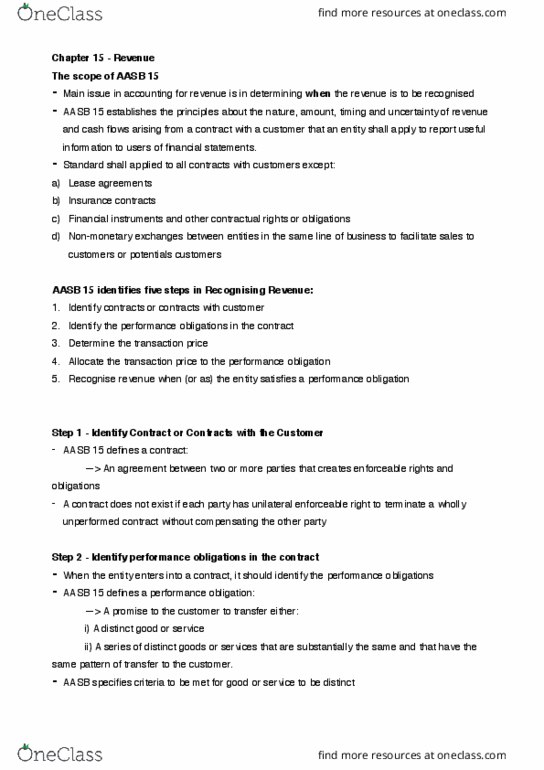

Revenue from contract with customers - ifrs 15: identify the contract with a customer. Each party unilaterally terminate contract without compensation. Not yet received and entitled to receive any consideration in exchange for promised goods/service. Recognize contract asset/liability depending on the entity"s performance and the customer"s payment relationship. Recognize unconditional rights to consideration separately as a receivable. Contract modification: change in scope or price or both approved by both parties. New contract (distinct promise goods/service, right to receive consideration reflecting the stand-alone selling price of promised goods/services) Contract modification: identify the separate performance obligations in the contract. Customer benefit from its use on its own or with readily available resources. Promise to transfer the goods/services is separately identifiable from other promises. Entity does not provide significant integration of the good/service with other promised goods/services the good/service does not significantly modify/customize another good/service. The good/service is not highly dependent on/integrated with other promised goods/service: determine the transaction price.