BUS 426 Lecture Notes - Lecture 8: Perpetual Inventory, Enquire, Cost Accounting

19 Sep 2012

School

Department

Course

Professor

Document Summary

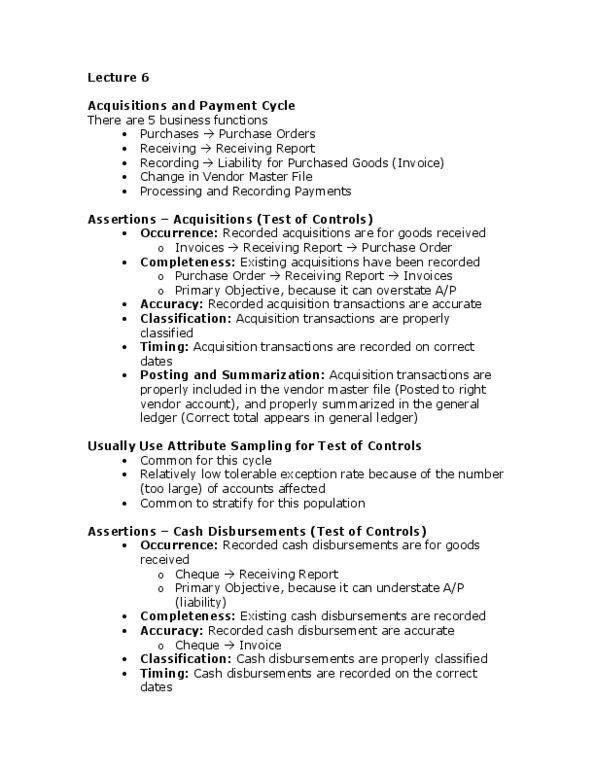

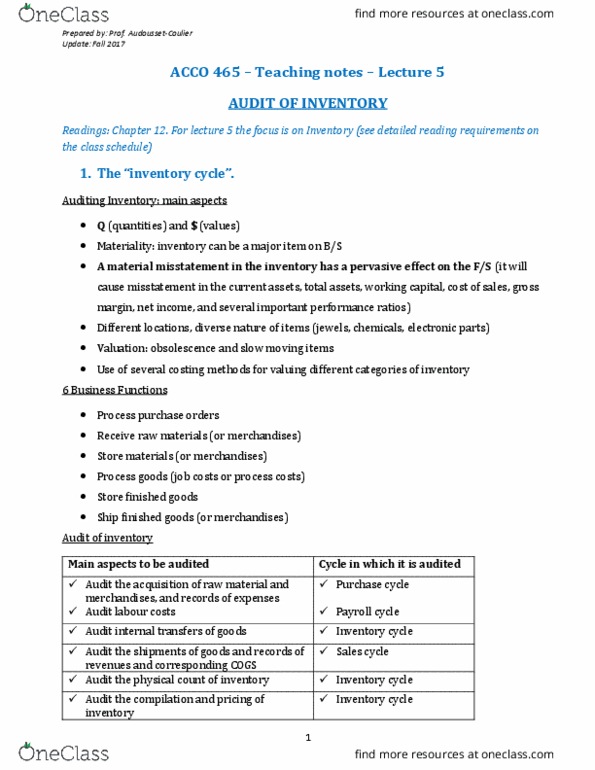

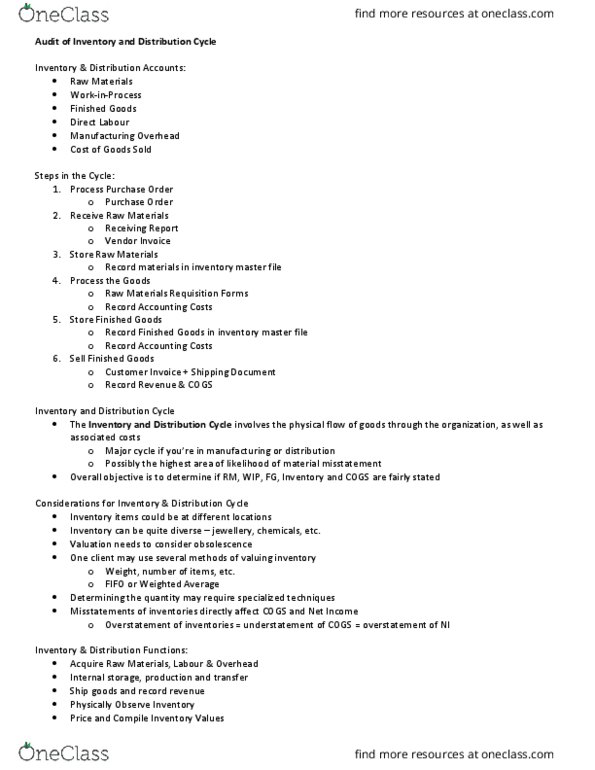

It may be a major item on the b/s. Inventory could be at a number of locations. Inventory could be made up of very diverse items (chemicals, electronics) Valuation can be tough, because of potential obsolescence. Client may use several methods for valuing the inventory. Process purchase orders acquisition + payment cycle. Shipping notice, shipping finished goods sales + collection. Varies more than other cycles, due to the wide variety of the types of inventory and in the level of sophistication required by management. Cost accounting controls are related to physical inventory and compilation of costs of that inventory from raw material to finished goods. Gross margin % of the prior year. Extended inventory value (price x quantity = cost) with prior year. Current year manufacturing cost with prior year: manufacturing cost could be: direct material, direct labor and manufacturing overhead.