ACCTG300 Lecture Notes - Lecture 1: Sole Proprietorship, Retained Earnings, Accounts Receivable

24 Jan 2016

School

Department

Course

Professor

Document Summary

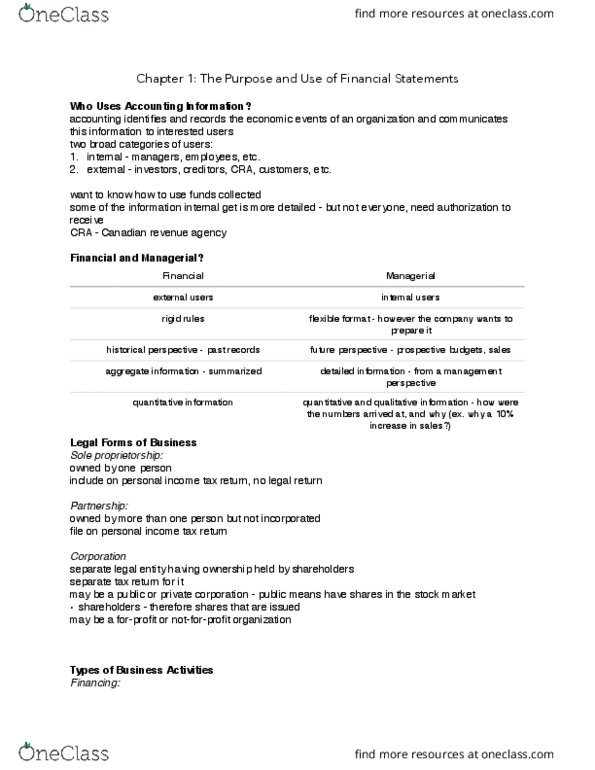

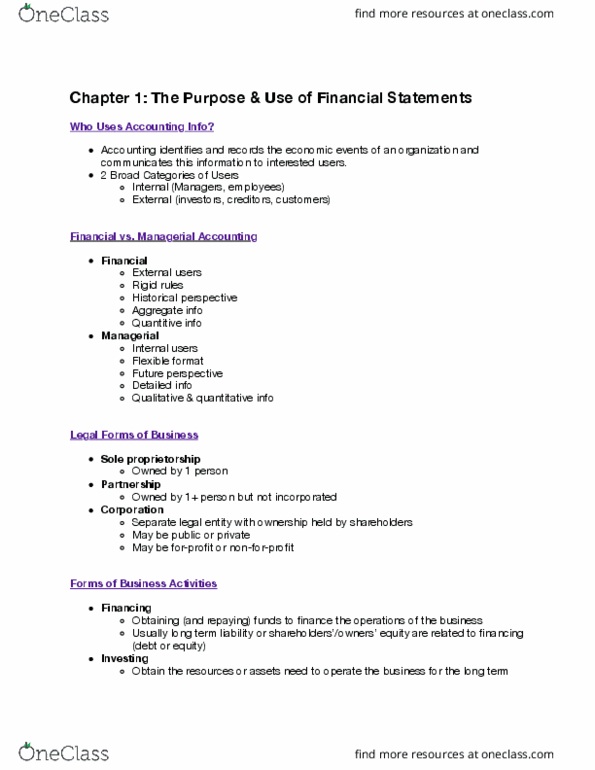

Legal forms of businesses: sole proprietorship owned by 1, partnership more than one but not incorporated. Negative if one quits = no business, unless dissolve: corporation separate legal entity third party. Separate everything bank account, tax return. Limited liability can"t sue individuals, only the. Types of business activities corporation: financing, investing, operating. Balance sheet: assets = liabilities + owers equity, at a point in time. Other annual report: annual reports publically traded must give shareholders, footnotes an annual report, management discussion, independent auditors" report must every year. B/s (balance sheet) own/owe (cash, common shares, I/s (income statement) made/lost in current year (advertising. Expenses, service revenue, sale, income tax expense, interest expense. Re (retained earnings) cumulative earnings (dividends, Asset expected to be converted to cash within one. Cash, short-term investments, accounts receivable, inventory, prepaid assets (ex. Asset not expected to be converted to cash within a year year. Long term investment, property, plant and equipment, intangible assets.