ECON101 Lecture Notes - Lecture 17: Marginal Product, Variable Cost, Fixed Cost

23 Apr 2017

School

Department

Course

Professor

99

ECON101 Full Course Notes

Verified Note

99 documents

Document Summary

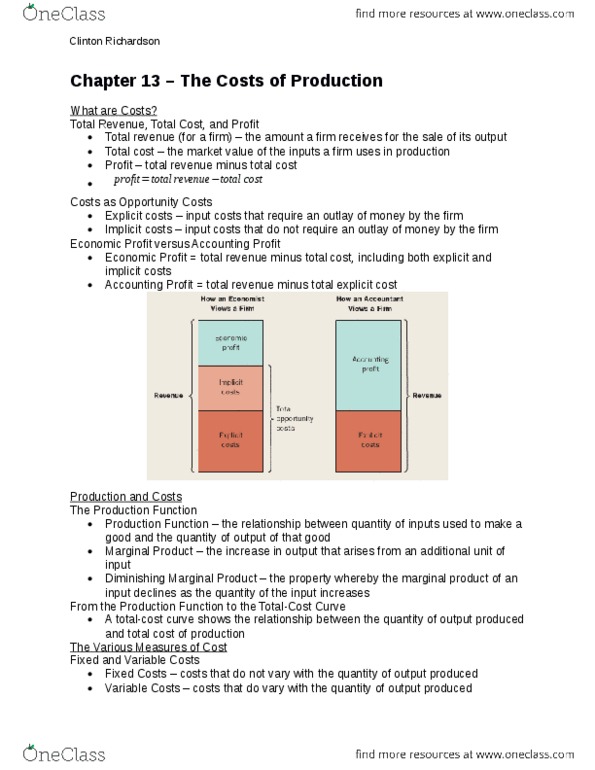

Inputs can be varied depending on your production needs. In the long run, all inputs are variable. = operating in the short run. (a quantity of a xed input can"t be changed in the short run) The total amount produced during some time period. Average product (ap) well have one of ap for every type of input (labour, capital, materials) The change in total product resulting from a change in the use of one input holding the quantities of all other inputs constant. What is the contribution of the next additional labour. The more you contribute, the more you add to production, eventually e ciency will decrease. The rm should be operating between the range of l*, l^ to be e cient. Accounting costs = include actual expenditures + depreciation expenses for capital equipment. (the more you use it, the more it loses value, it depreciates) are explicit costs. Economic costs = accounting costs + opportunity costs.