AFM102 Lecture Notes - Lecture 5: Financial Statement, Ratia, Retained Earnings

15 Oct 2015

School

Department

Course

Professor

Document Summary

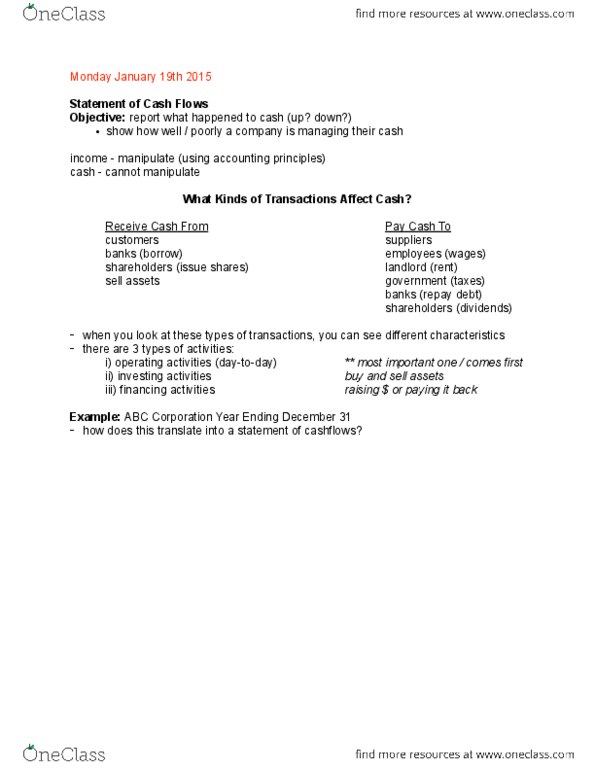

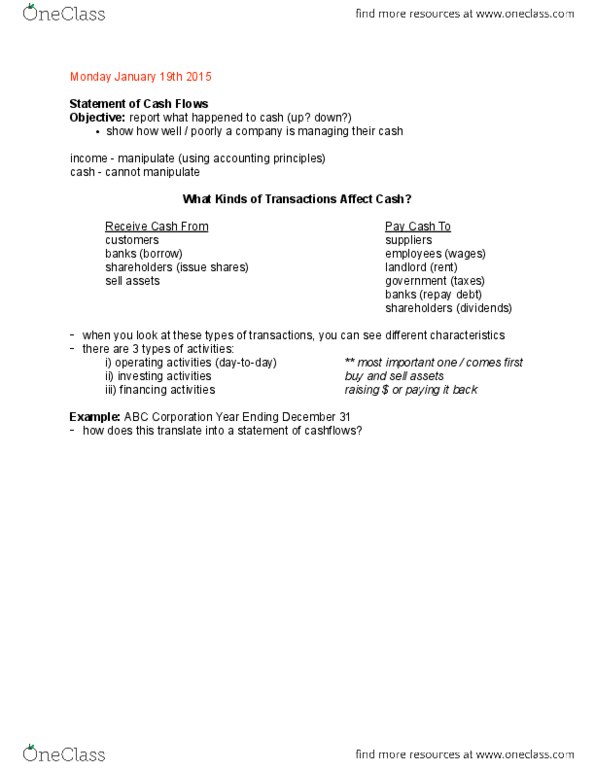

3 types of activities: operating activities investing activities (buy/sell assets) Compare results (including all line items) to same company over time. Therefore, financial statements have features to make them more useful: comparative financial statements. Each f/s will have minimum of two columns, often more so that when we have sales we would have multiple comparative figures. Operating income (sales- cost of goods sold- selling expenses- admin. Core of the business and it is recurring. Other gains (sell assets), other expenses (flood for example) Income before income tax expense (not all companies pay the same rate: classified balance sheet. Group accounts into sub- categories (sub-totals) that are helpful to users. Ratio analysis (3 today, more to come: debt to assets raito. Business background if banker calls loan, company usually out of business. Debt to assets = total liabilities / total assets. Higher the ratio, the riskier the company: asset turnover ratio.