AFM123 Lecture Notes - Lecture 3: International Financial Reporting Standards, Retained Earnings, Financial Statement

26 Oct 2015

School

Department

Course

Professor

Document Summary

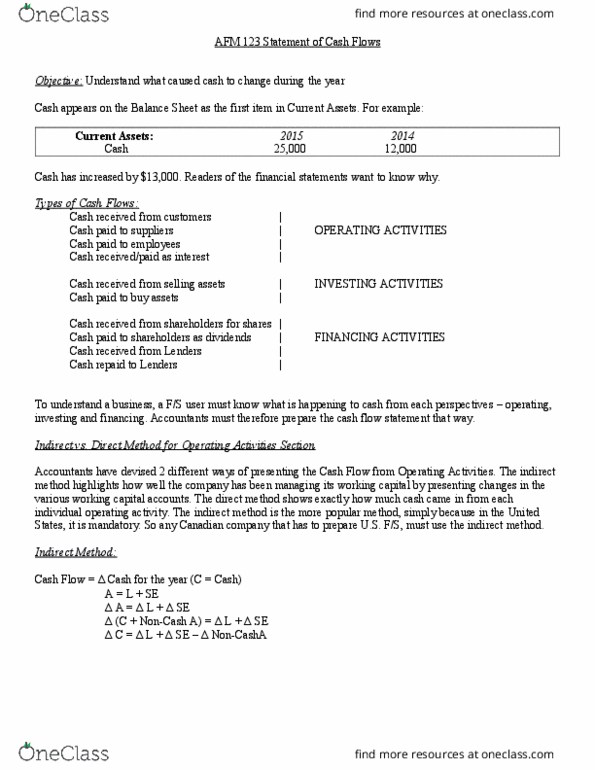

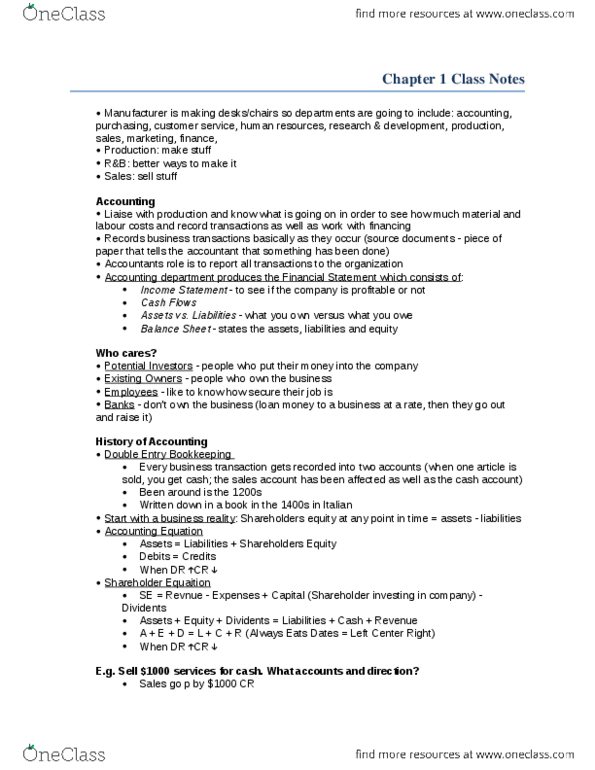

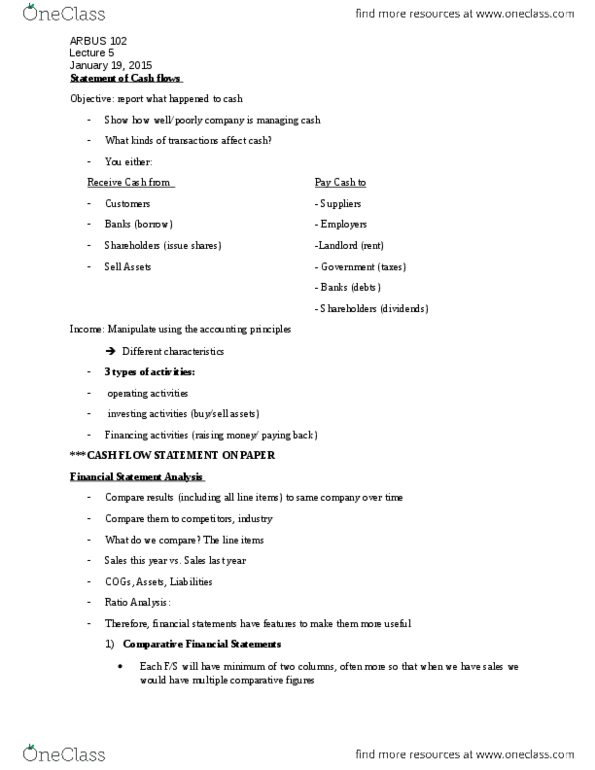

Objective: report what happened to cash (up? down?: show how well / poorly a company is managing their cash income - manipulate (using accounting principles) cash - cannot manipulate. Receive cash from customers banks (borrow) shareholders (issue shares) sell assets. Pay cash to suppliers employees (wages) landlord (rent) government (taxes) banks (repay debt) shareholders (dividends) When you look at these types of transactions, you can see different characteristics. ** most important one / comes first buy and sell assets raising $ or paying it back: operating activities (day-to-day, investing activities, financing activities. What are bankers, investors, governments (people who care about these f/s) going to. In conclusion, financial statements have features to make them more useful. Each f/s will have a minimum of 2+ columns as comparative figures: comparative financial statement figures sales operating exp. net income (less) 8,000 assets cash etc: multi-step income statement. Operating income (sales - cogs - selling expenses - administrative expenses)